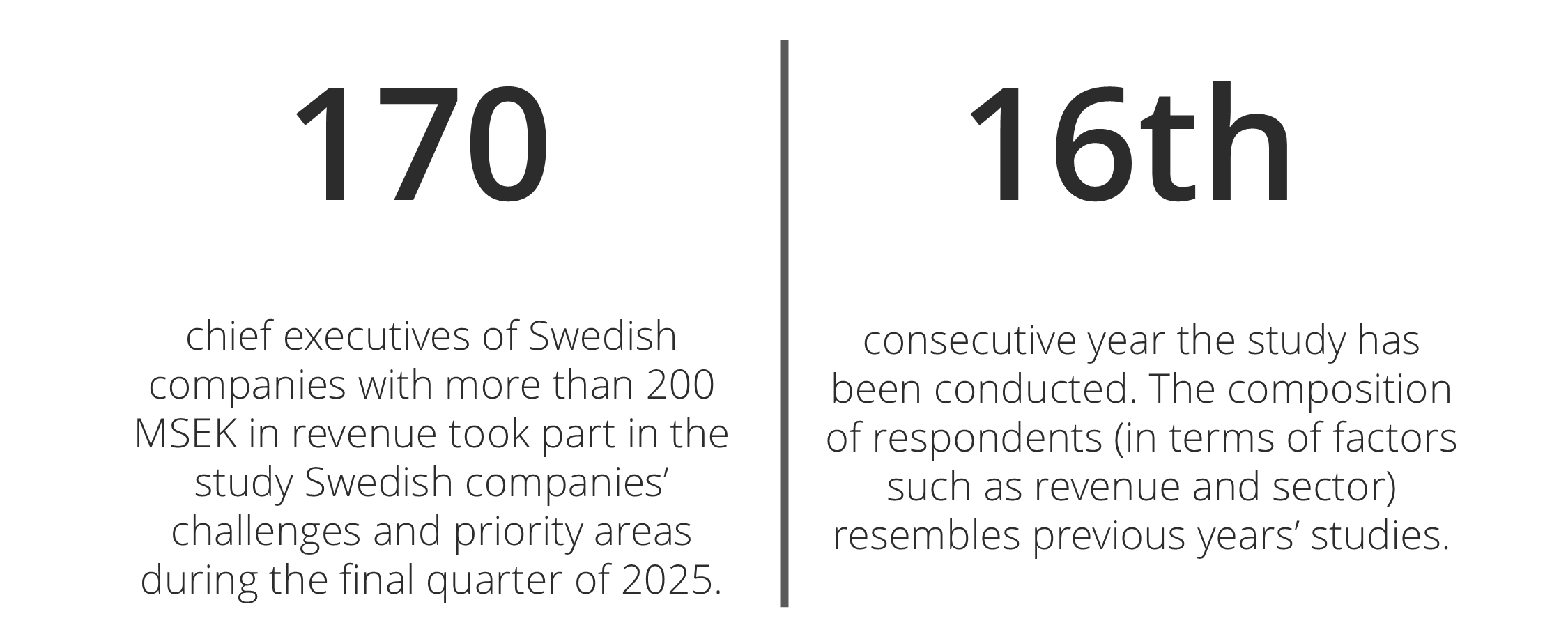

Axholmen’s CEO Study 2026 shows, in line with last year’s findings, clear optimism about the macroeconomic outlook. Lower inflation and signs of stronger growth are contributing to a more positive view, although some concern remains linked to political uncertainty and the geopolitical situation. Taken together, this is driving greater willingness to invest and a shift towards growth rather than cost-cutting, with concrete growth strategies and pricing continuing to be decisive.

Swedish companies' challenges and strategic priorities in 2026

Summary

Swedish chief executives remain optimistic ahead of 2026, in line with the previous year. Lower inflation and higher GDP are contributing to brighter prospects, although external factors are dampening confidence in the global recovery

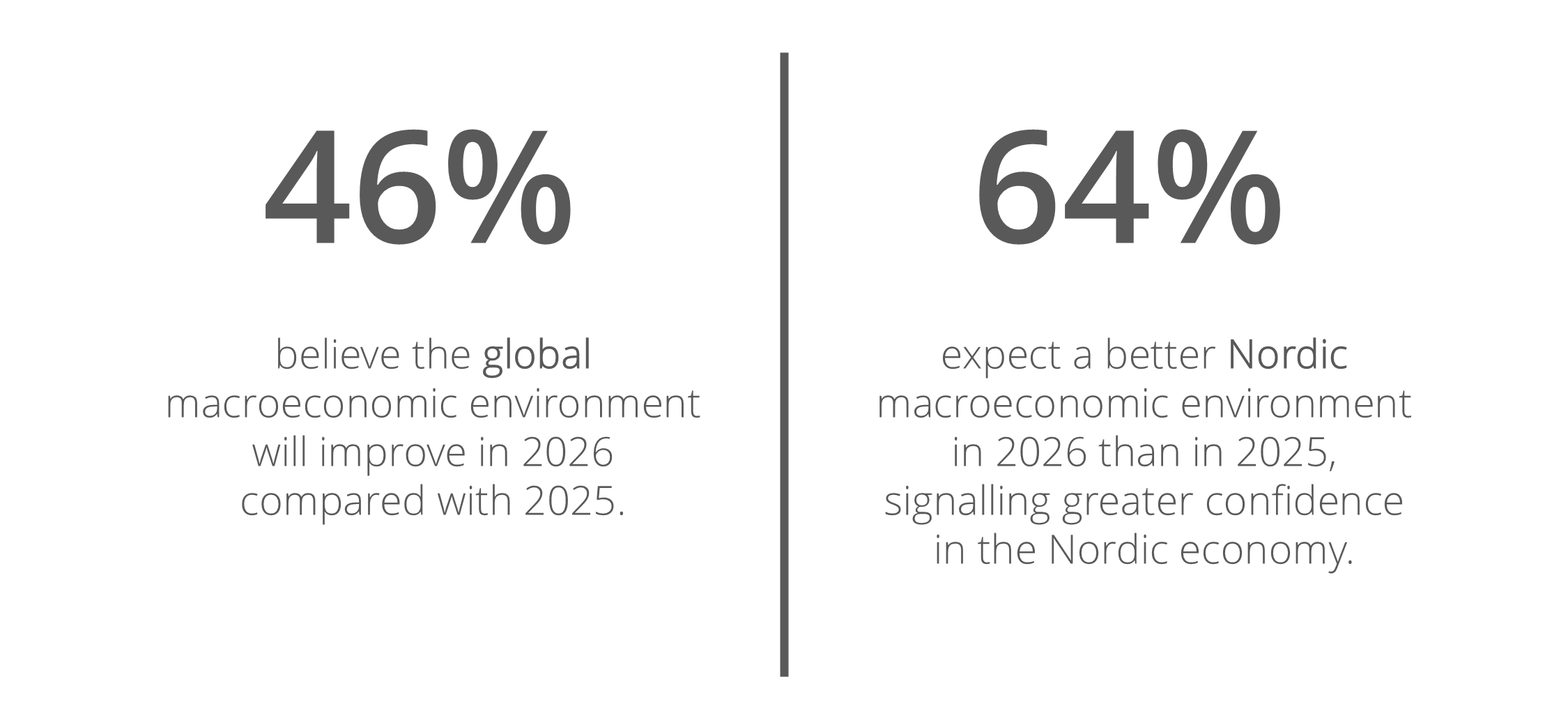

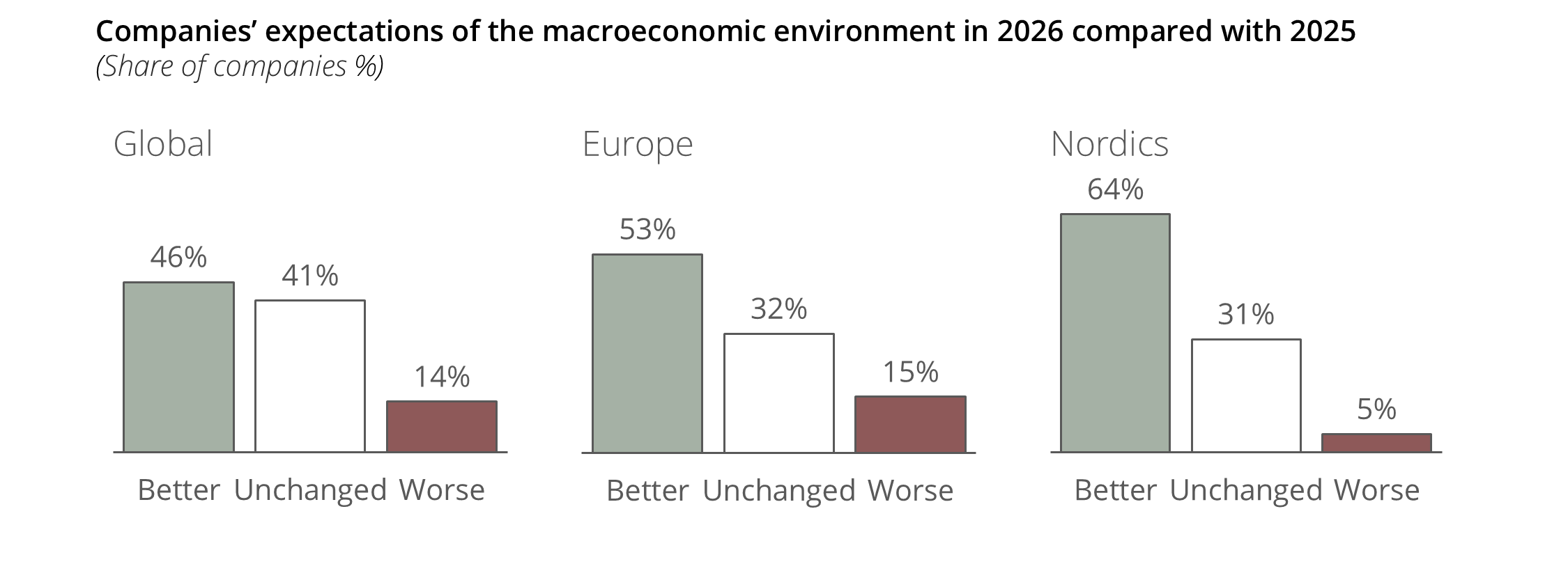

Chief executives believe the global macroeconomic situation will improve in 2026 compared with 2025. Only 14% expect a decline, while the remaining respondents foresee an unchanged outlook.

of the surveyed business leaders see growth initiatives as more important than cost efficiencies ahead of 2026, with a focus on developing goods and services and on sales.

of companies expect a 0% net effect from US tariffs, indicating that most companies plan to offset the impact, for example by rerouting supply chains, making price adjustments or contract adjustments.

of chief executives state that their companies have already achieved lower costs through the use of AI, primarily through increased process automation and streamlining of administrative tasks.

Swedish chief executives are positive ahead of 2026; most expect a better economic environment both in Sweden and globally. The backdrop is a global economy with moderate but stable growth, while Sweden remains in a downturn but is expected to recover.

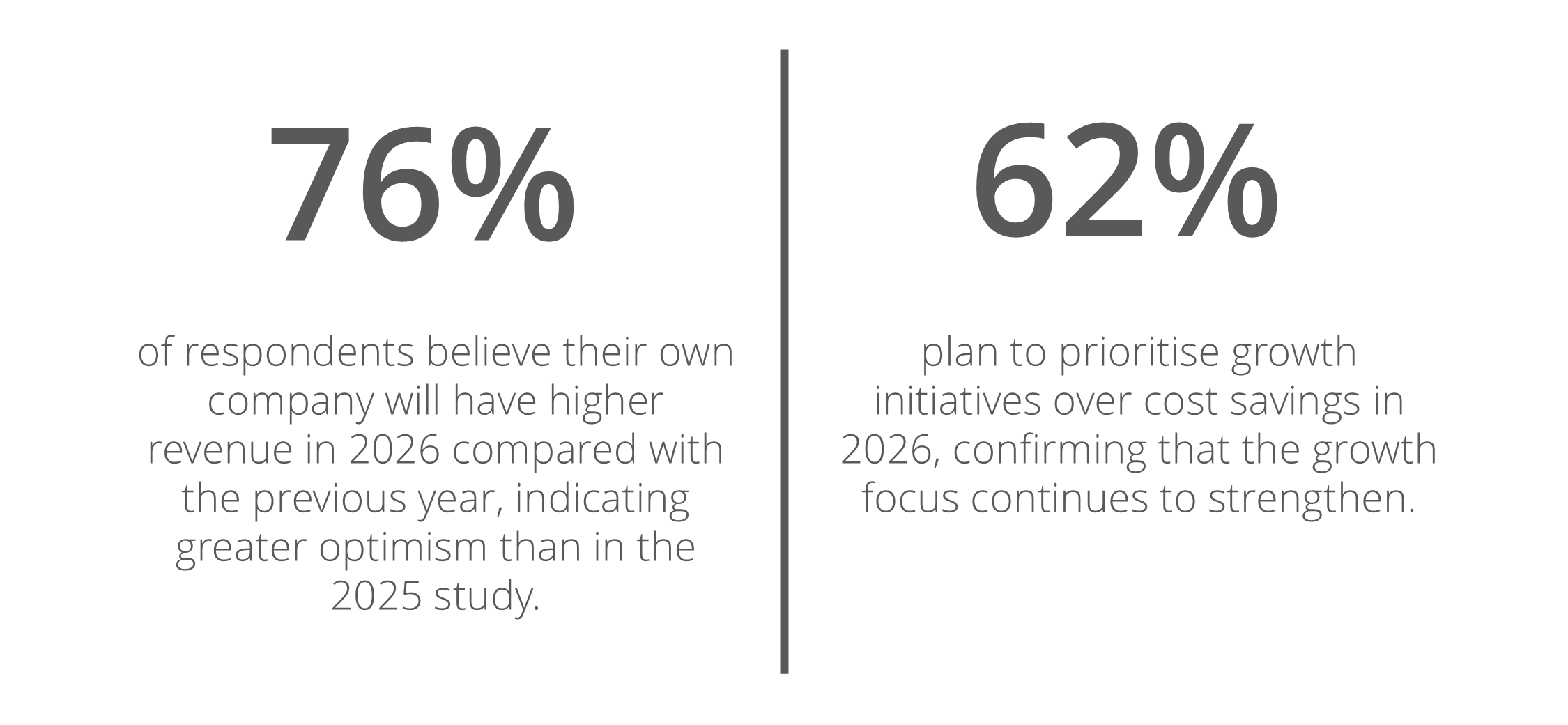

Three in four expect higher revenue in 2026 for their own company, and a majority will prioritise growth initiatives over cost savings, confirming a continued more offensive corporate agenda.

Companies are signalling a clear shift towards turning AI into tangible impact; tariffs and trade barriers are dampening confidence in global growth; and Agenda 2026 sets out which priorities will dominate the chief executive agenda for the year.

When global growth is not a given, sharp prioritisation and strong execution capability become decisive; structured pricing and a clear growth agenda become central tools for creating profitable growth.

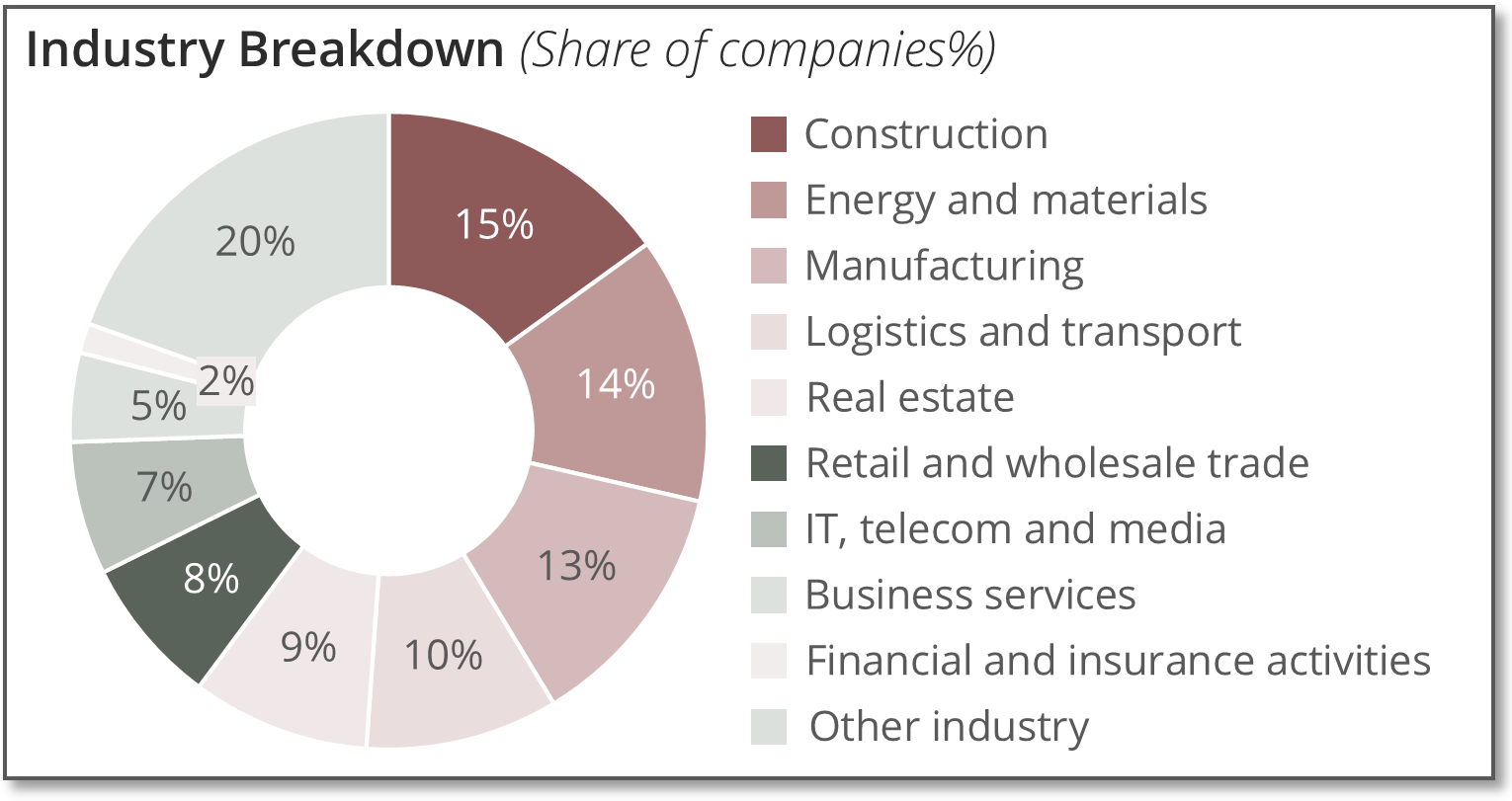

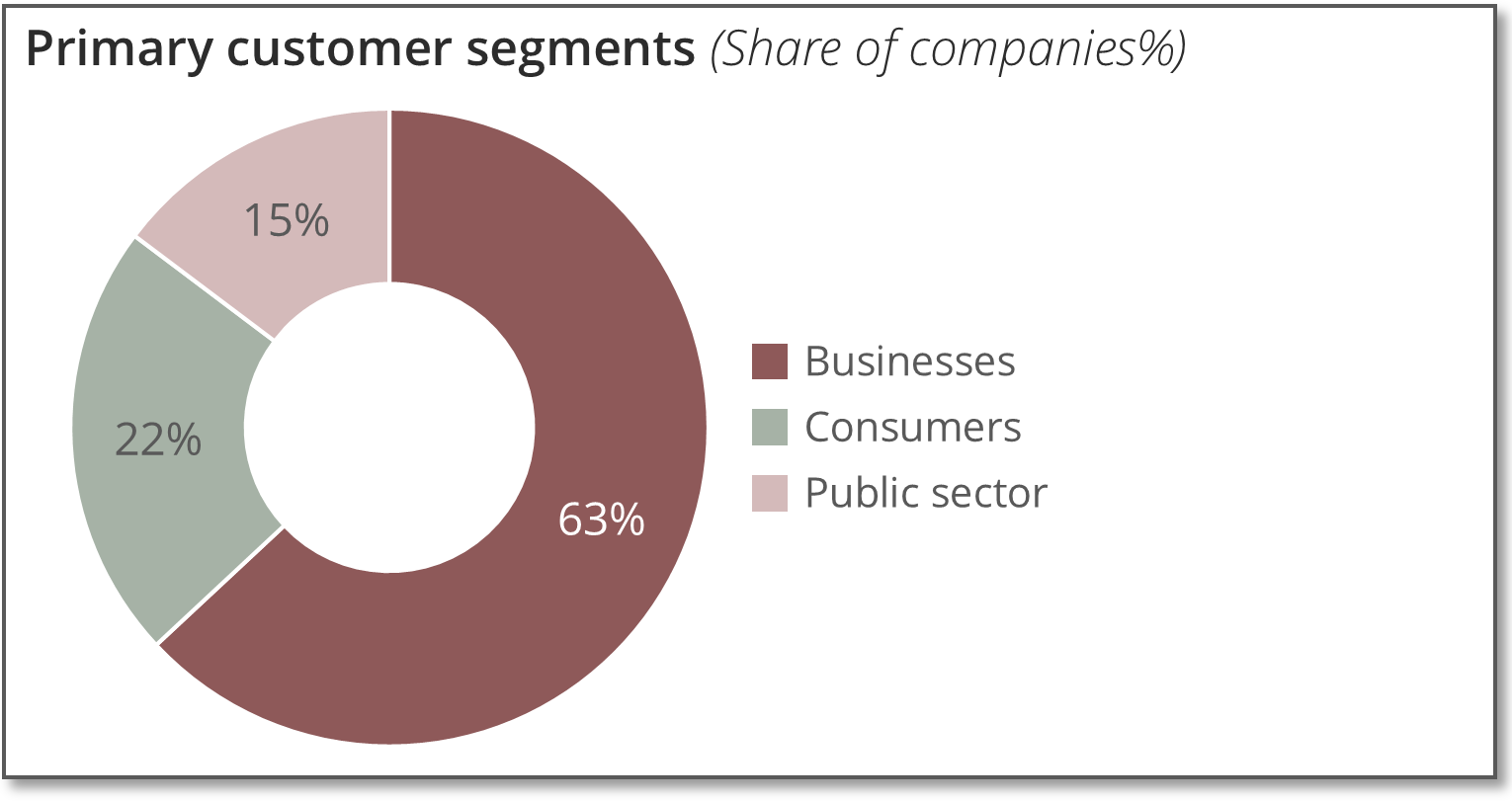

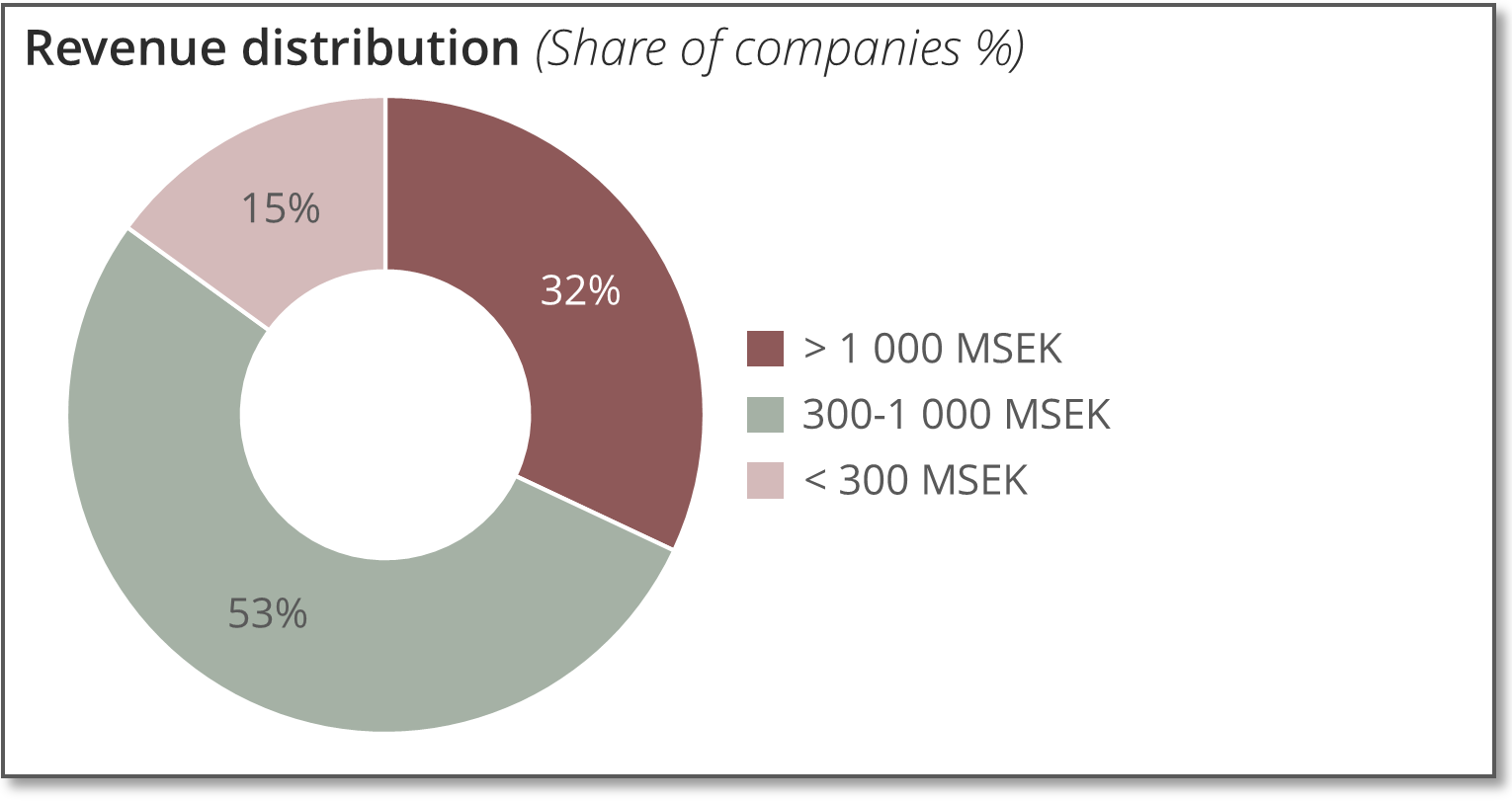

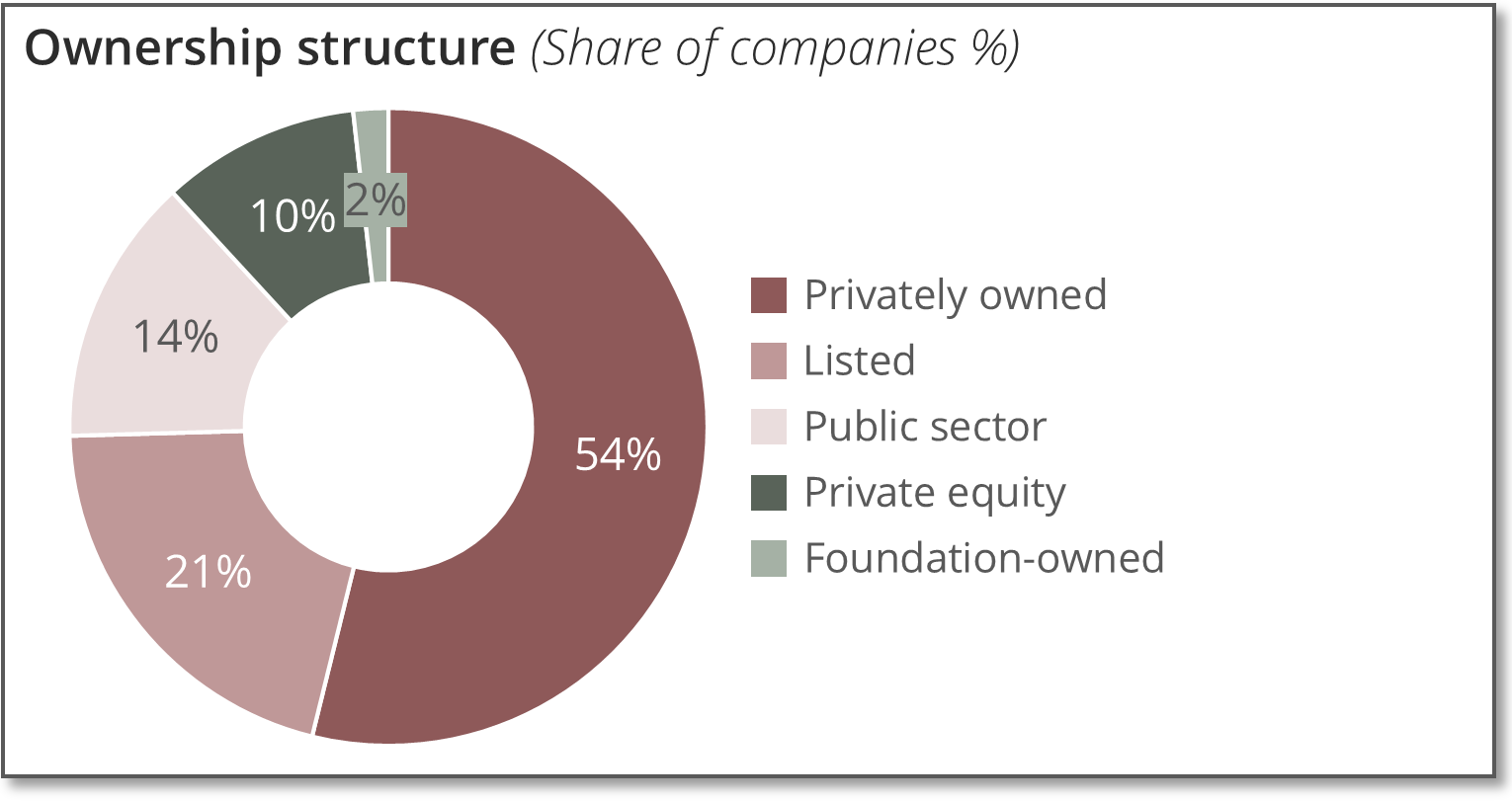

The respondents

Overview of the responding companies; the composition is similar to previous years

Global

Growth expectations remain, and confidence in the macro-outlook is holding up ahead of 2026 - Swedish chief executives are particularly optimistic about the Nordic economy

”2025 has been marked by many uncertainty factors; 2026 will be somewhat better in that respect”

Fredrik Ekström, Maven Wireless

”The policy rate is moving downwards, the figures point to an economic recovery, large stimulus packages.”

Jon Widell, Kyl- och Frysexpressen

> Global growth is expected to ease slightly but remain around moderate levels. Global GDP growth is forecast at 3.2% in 2025 and 3.1% in 2026, with around 1.5% in advanced economies and just over 4% in emerging market and developing economies. This is marginally stronger than the IMF’s April forecast, but weaker than projected before the latest policy changes and trade tariffs. The IMF also highlights that the world economy is entering a period of more persistent fragmentation, with bloc formation and major climate investments, which could weigh on trade and productivity.1)

> Global inflation is expected to continue easing, but remain above target in the US while being low in many other advanced economies. Conditions are characterised by higher US tariffs, new trade agreements, and companies that have partly mitigated the effects by rerouting supply chains.

Especially in Sweden, expectations of an improvement in growth are high — rate cuts, lower inflation and ambitious stimulus for households will increase demand during 2026… Globally it looks more stable, and we believe growth will remain just over 3% this year.”

Johan Javeus, Chief Strategist SEB

1) IMF World Economic Outlook, October 2025

Optimism is highest in the Nordics and Europe. Expectations for global growth are more subdued, consistent with forecasts pointing to a stabilising environment

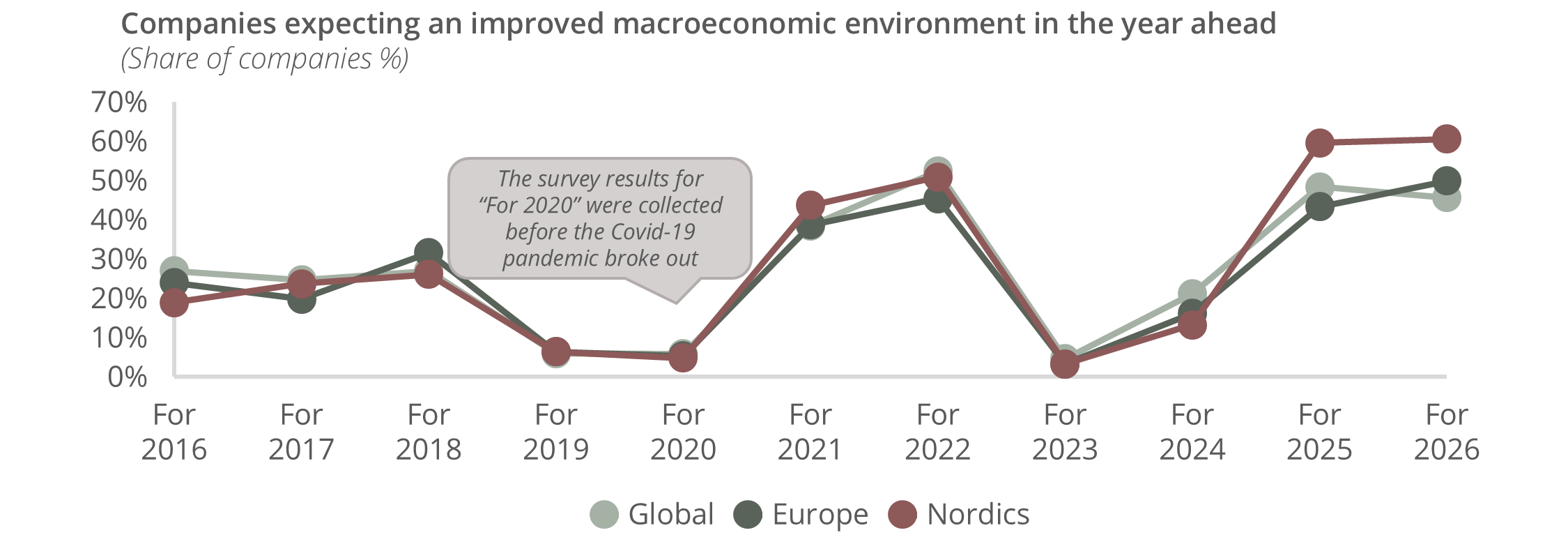

The forecast for global economic development points to stabilised levels of GDP growth around three per cent from 2026 onwards…

…which is also reflected in chief executives´view of the macroeconomic climate: markedly more optimistic than in 2023 and 2024, but roughly the same as in 2025.

> Forecasts indicate that global GDP growth has stabilised at around 3 per cent since 2024, corresponding to a more normal growth environment after recent years’ volatility.

>Chief executives’ expectations for the macroeconomic situation ahead of 2026 are markedly more optimistic than ahead of 2023–2024 and are in line with assessments ahead of 2025, signalling an expectation of gradual improvement in the economic cycle.

1) IMF World Economic Outlook

Sweden

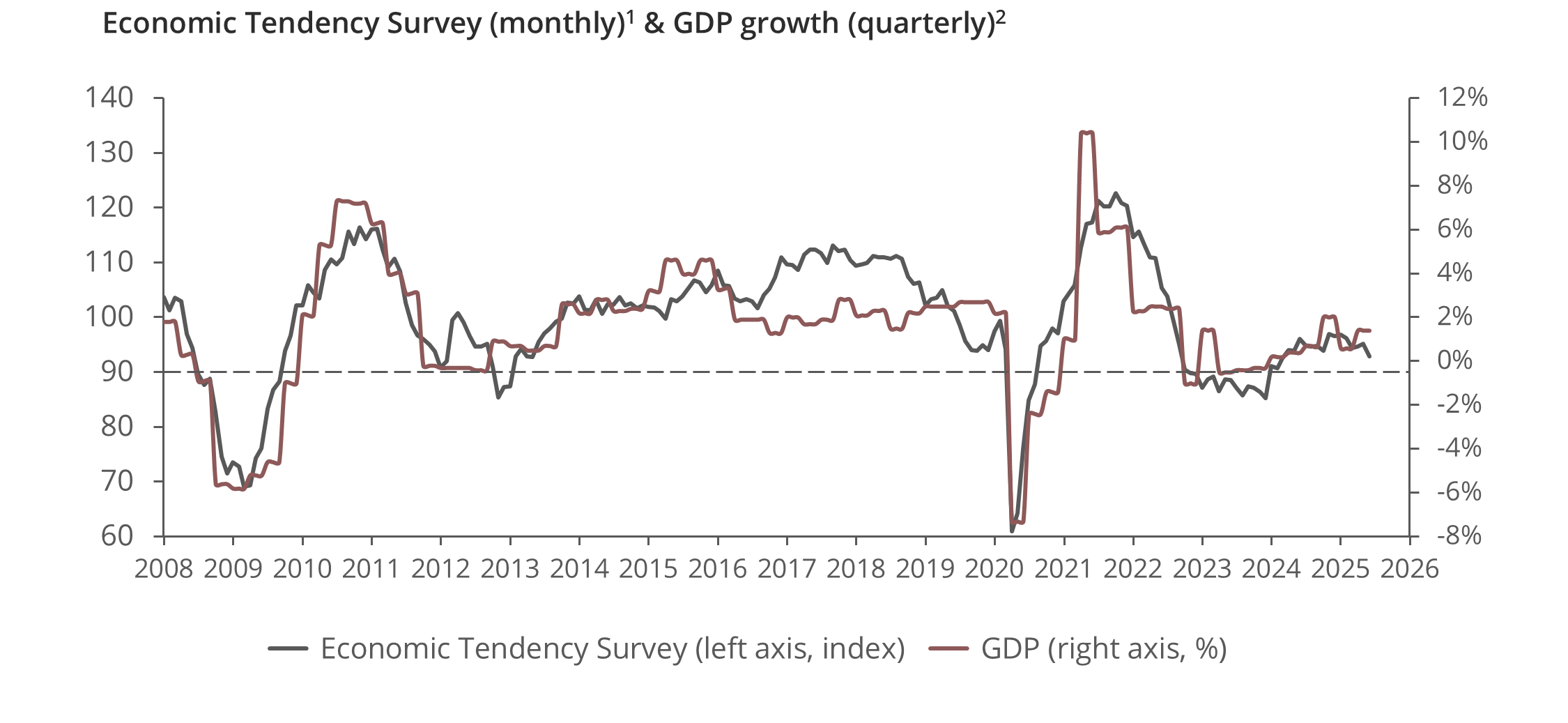

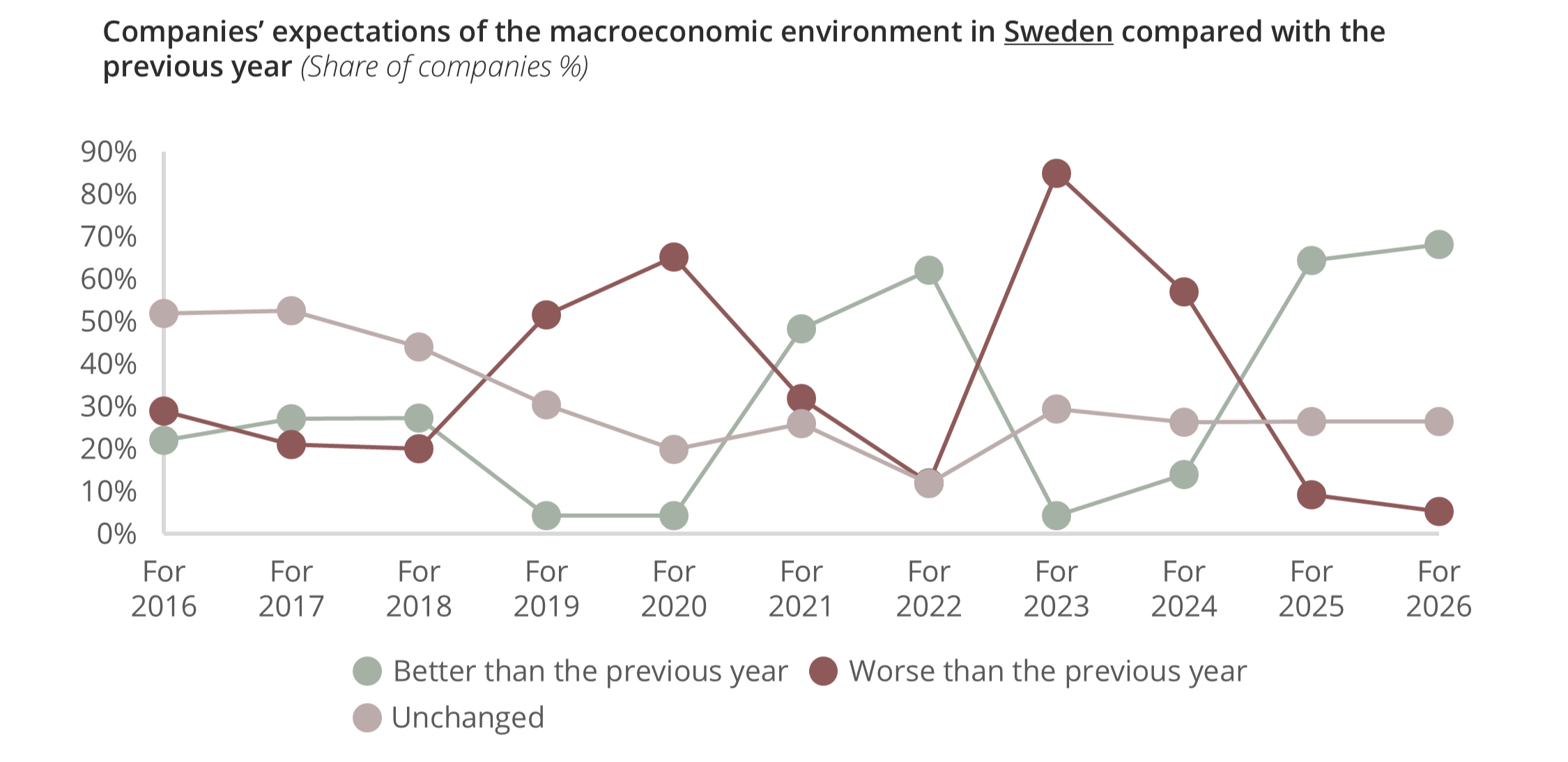

The Economic Tendency Survey remains weak, but Swedish chief executives continue to expect Sweden’s macroeconomic conditions to be stronger in 2026 than in 2025

Sentiment around the economy has improved during 2025, even though the cycle remains weak and fell short of chief executives’ expectations for the year…

1) Konjunkturinstitutet

2) SCB

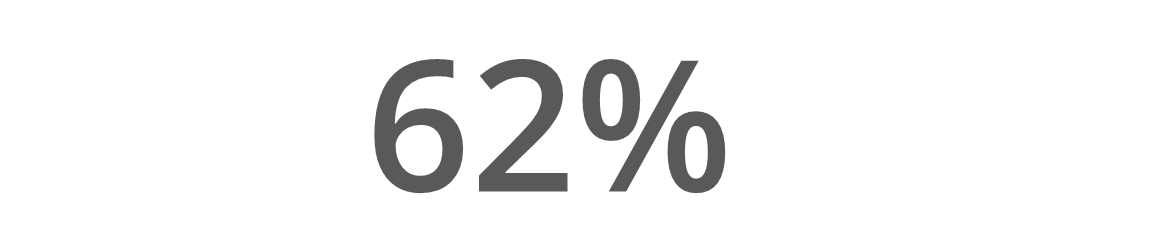

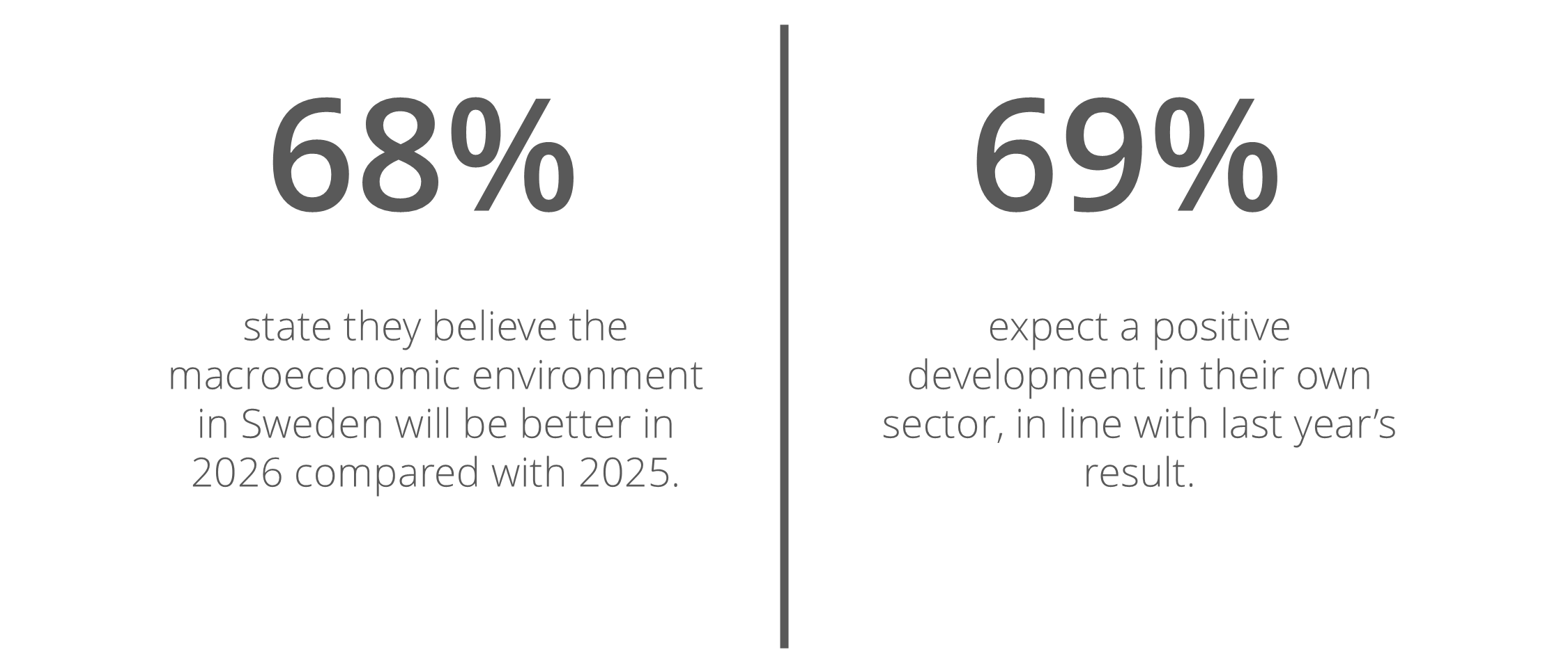

…however, chief executives have high expectations for the Swedish macroeconomic climate, with almost 70% believing 2026 will be better than 2025.

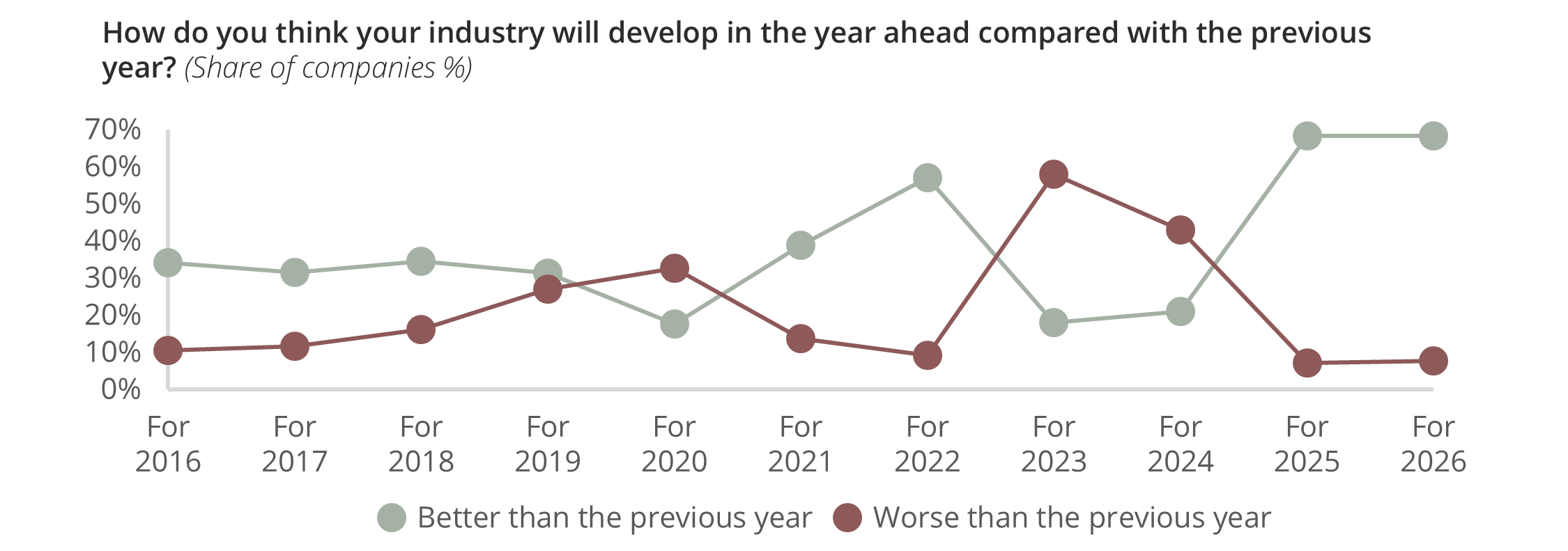

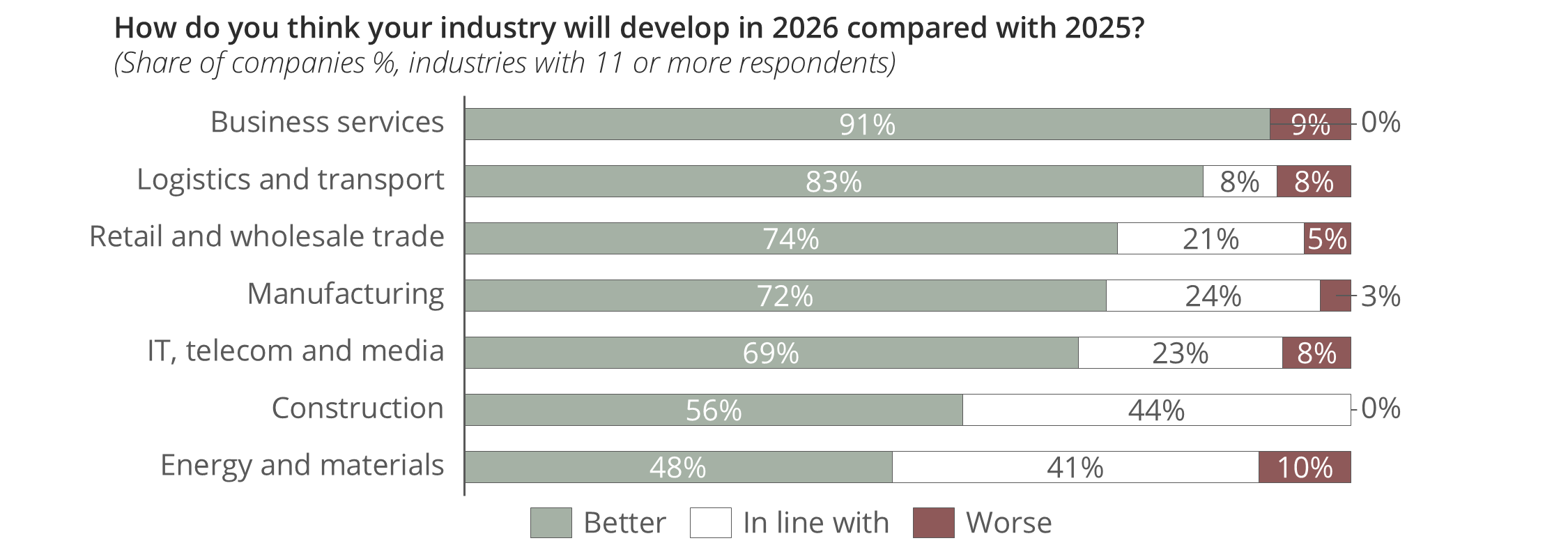

Confidence in the economy is also reflected in expectations for their own industry, where the overall view is strongly positive, even if it varies somewhat between sectors

The number expecting positive development in their own industry ahead of 2026 is the highest level so far…

> Chief executives remain optimistic about their own industry ahead of 2026, as they were ahead of 2025, and at significantly higher levels than previous years.

…but there are clear differences between industries.

> Business services, where over 90% of respondents believe in positive development, has the most optimistic outlook ahead of 2026.

> Construction and the energy sector are more cautious than others, which may be linked to the delayed effects of rate cuts, even though they are markedly more positive than ahead of 2023 and 2024.

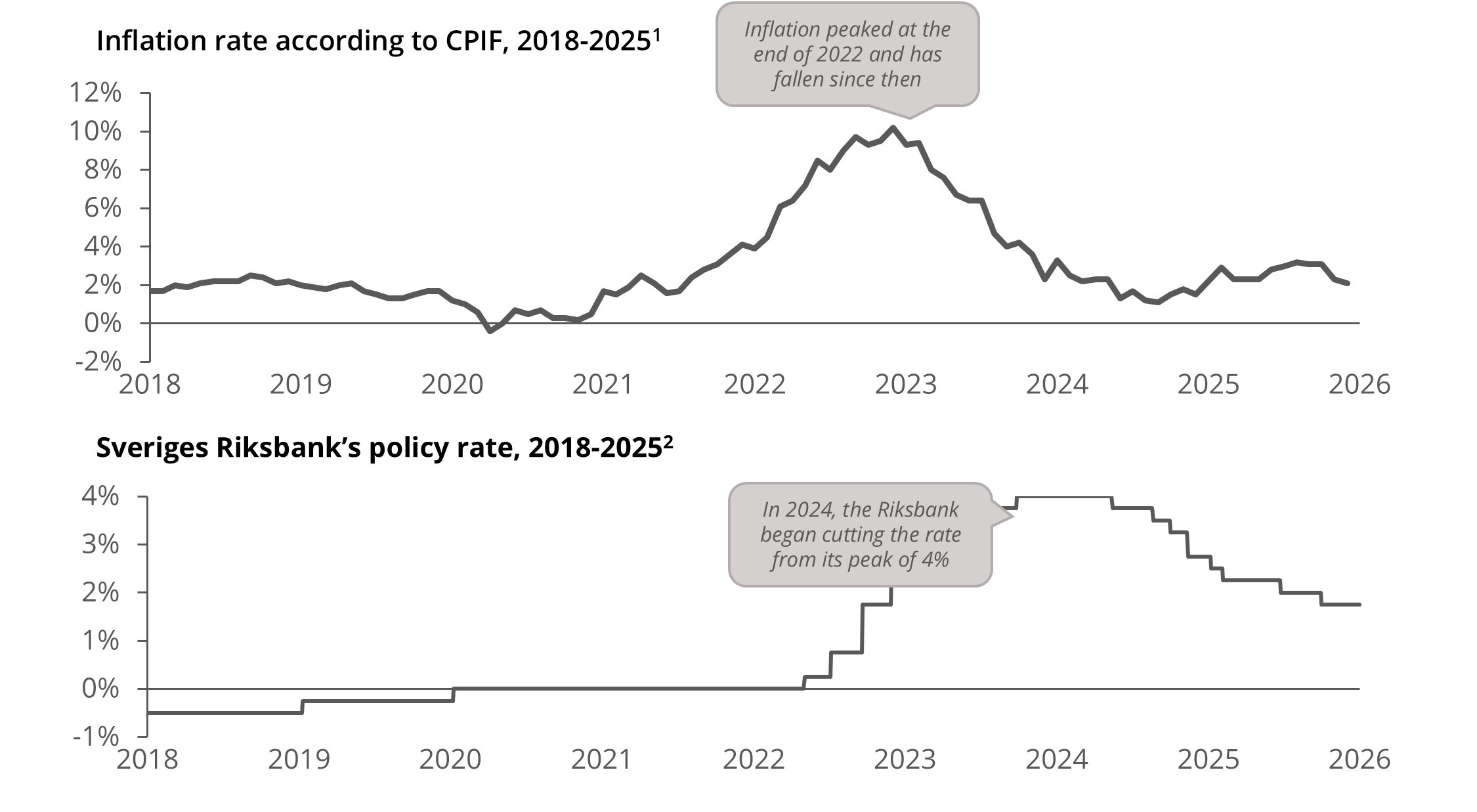

While the policy rate and inflation have both declined over the past year, they remain above pre-pandemic levels, and the National Institute of Economic Research estimates that the downturn will last until 2028

Inflation has risen again during 2025, although at far lower levels than in 2022 and 2023.

”The US administration’s policies, and in particular the trade war, have created great uncertainty in the world economy. That also has effects in the Swedish economy. The recovery we saw last autumn has been broken and the downturn more prolonged.”

Elisabeth Svantesson, Minister of Finance, 24 June 2025

> The Swedish economy has improved during 2025 but has continued to be in recessionary conditions, which Konjunkturinstitutet calculates will not be over until 2028. Sveriges Riksbank has gradually adjusted the policy rate downwards and inflation has risen during the year, ending the year just below the 2 per cent target.

> Swedish GDP growth in 2026 and 2027 is expected to be driven mainly by household consumption and a higher pace of investment. At the beginning of 2026, the labour market is also expected to begin recovering after a couple of difficult years.

1) SCB, Statistiska centralbyrån

2) Sveriges Riksbank 2025

External factors

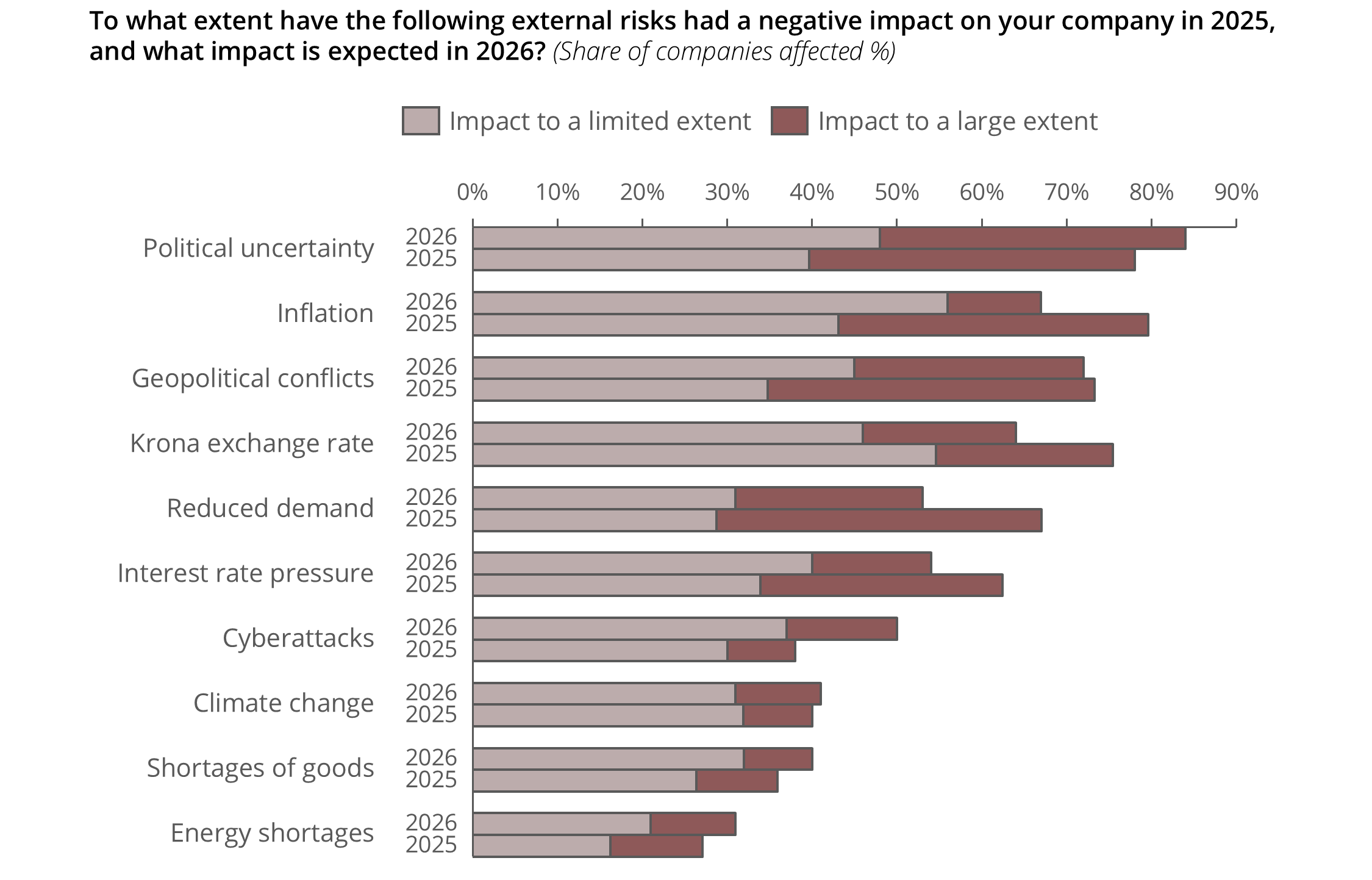

The study indicates that external factors are expected to be less negative than in previous years - largely due to lower inflation and interest rates - while global political uncertainty is expected to have a greater impact

During 2026, Swedish chief executives expect some easing in economic risks, but see growing challenges linked to global tensions.

”The security policy situation is driving growth.”

CEO, Manufacturing industry

”Political decisions in the short term, which also creates opportunities.”

Tobias Moberg, Moberg Bil

”Access to capital in the market will affect business to a much greater extent than any of the above, as it always does regardless.”

Adam Källberg, Auburn Holding AB/AD Sverige AB

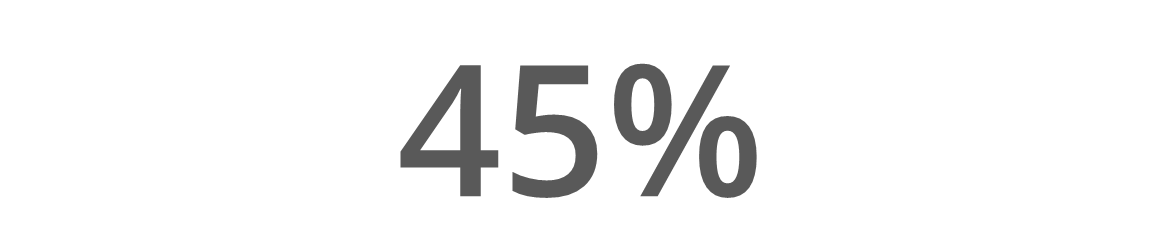

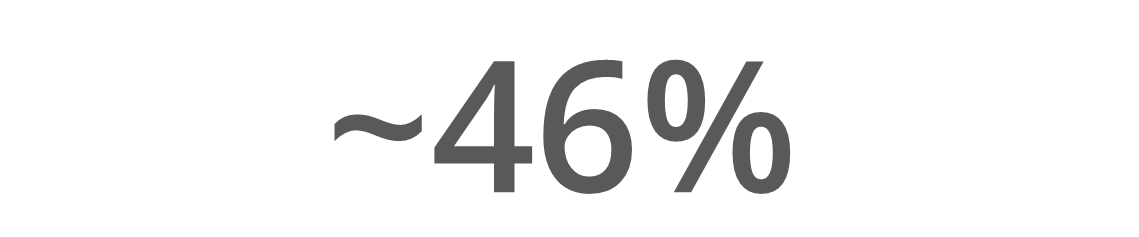

> Overall, almost half of companies report that in 2025 they were affected to a large extent by increased interest-rate pressure, while only 14% say they expect a corresponding impact in 2026. Inflation is also declining clearly, from 45% to 11%, and the share that sees reduced demand as a major risk falls from 46% to 22%. At the same time, slightly fewer companies state that political uncertainty is expected to have a large impact. Overall, this points to a marked easing in economic and political risks ahead of 2026.

> For other external factors, such as climate change, cyberattacks and energy shortages, the impact to a large extent remains at roughly the same level as the previous year.

”Fundamentally, in Sweden it largely comes down to the household sector and the trajectory of consumption, which will drive growth. Internationally, it is more about how resilient the global economy is, the development of energy prices, and geopolitical conflicts. Geopolitics is incredibly difficult to assess, with risks on both the upside and the downside. Peace in Ukraine, the risk of a trade war between the EU and China, and what Trump does next could have major consequences.”

Johan Javeus, Chief Strategist SEB

Companies

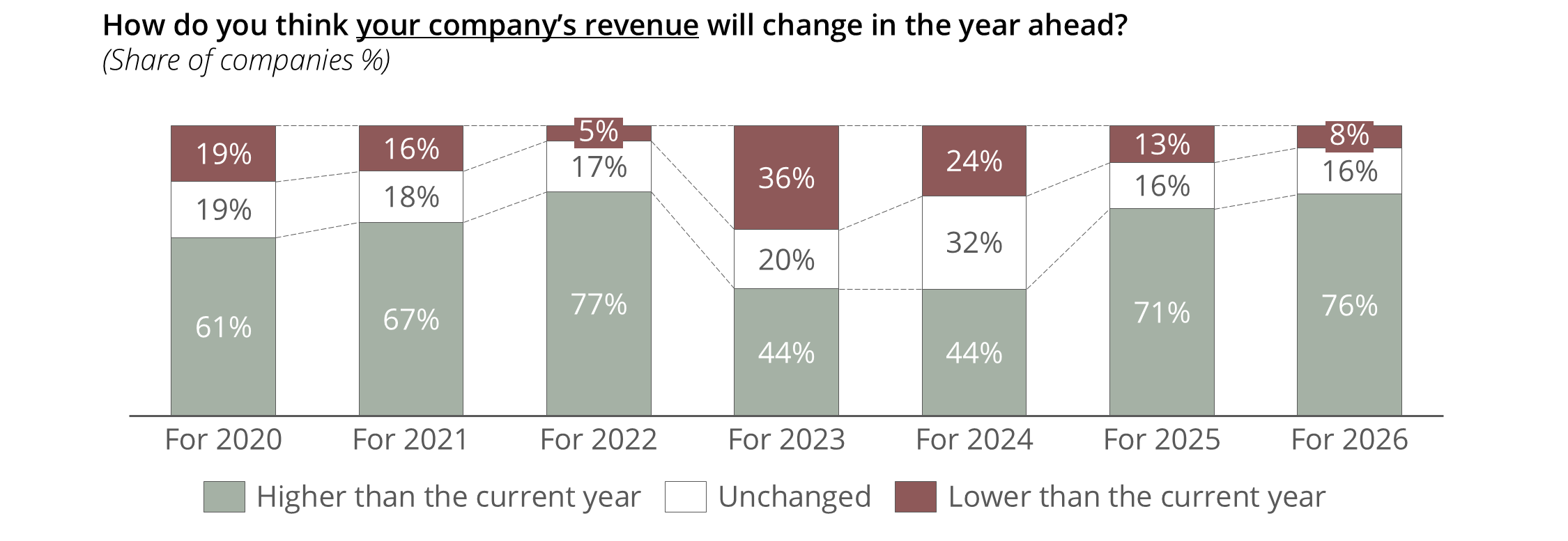

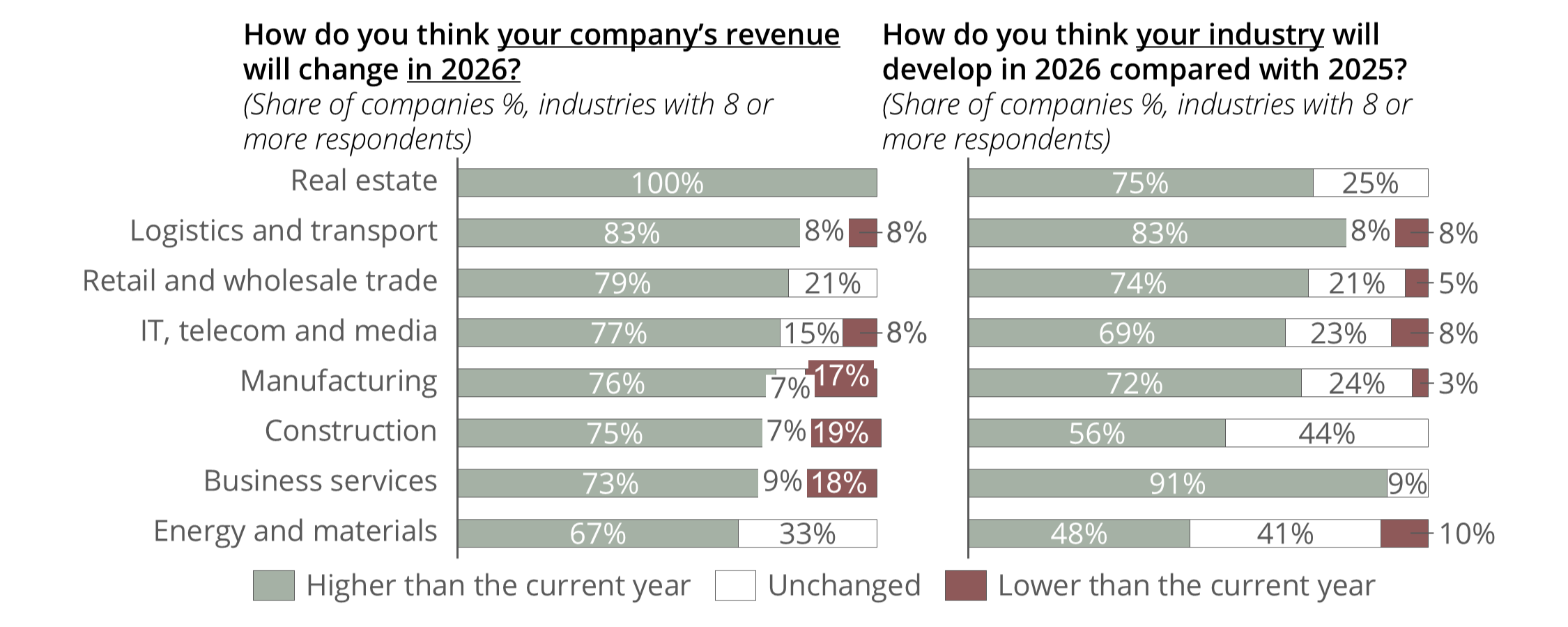

Respondents are very optimistic about revenue growth in 2026 compared with 2025, and are generally more confident in their own company’s outlook than in the outlook for their industry

The number who expect higher revenue in their own company ahead of 2026 is the second-highest over the past 7 years…

> Optimism is back at a high level and most companies expect rising revenue next year, but history shows that conditions can turn quickly if uncertainty increases.

…but optimism differs between industries, and between views of their own company compared with the industry.

> In property, construction and energy, several companies believe their own company will perform better than the industry in 2026, which in practice means they must take market share, not just grow with the market.

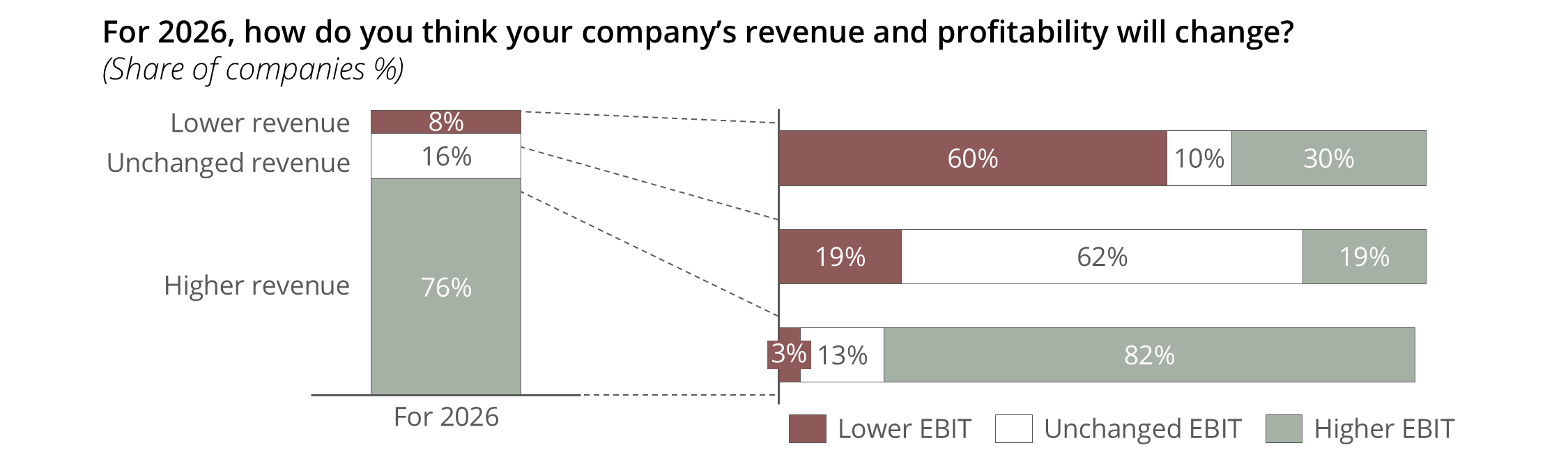

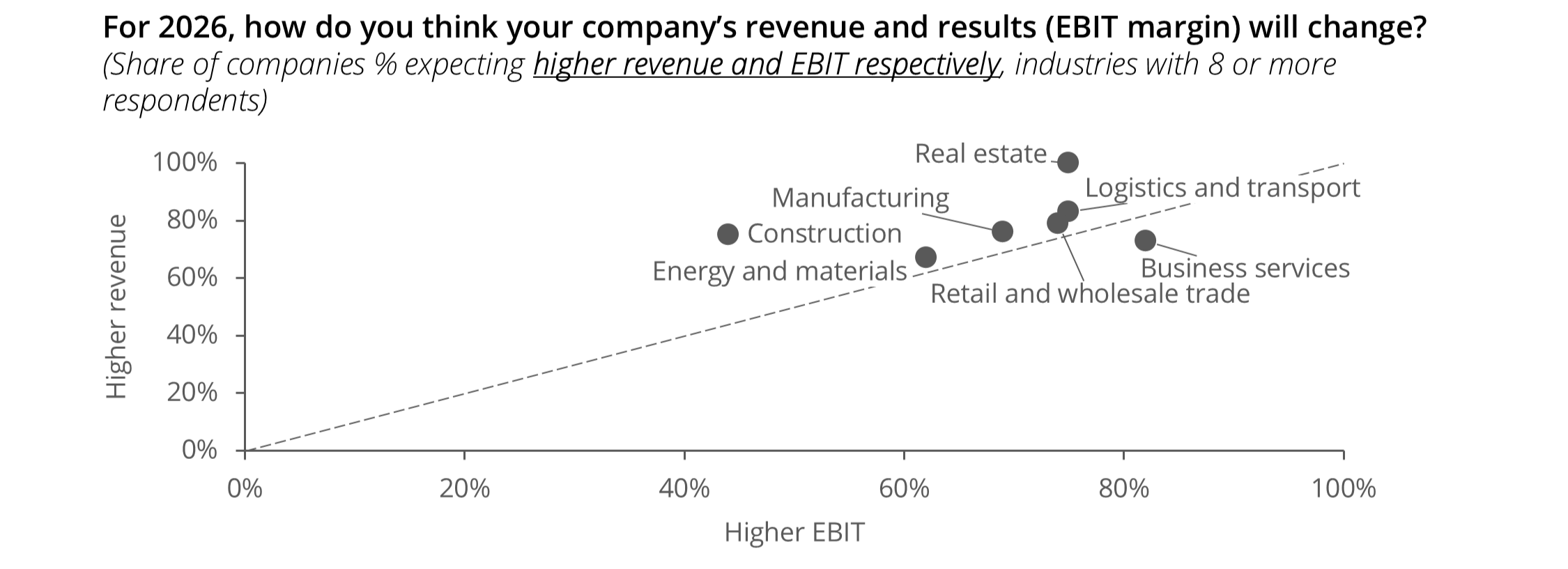

Expectations of higher revenue correlate with more optimistic expectations for margins, although the picture varies across industries

A strong majority of Swedish chief executives have a positive expectation for 2026, with 76% expecting higher revenue for their own company…

> There is a correlation between respondents’ expectations for revenue and profitability, where higher revenue is associated with higher margins and vice versa.

> What stands out is that 30% of companies that expect lower revenue still expect higher EBIT, which may be because they anticipate margin uplift through price increases, efficiencies or a better mix, or that they deliberately scale back unprofitable business.

…but there is also variation between industries as to whether revenue or profitability will be most affected.

> As in 2025, respondents believe that the turnaround during 2026 will primarily drive increased revenue rather than improved margins.

> The services sector stands out, with respondents believing margins will increase to a greater extent than revenue, which is reasonable in a less capital-intensive sector.

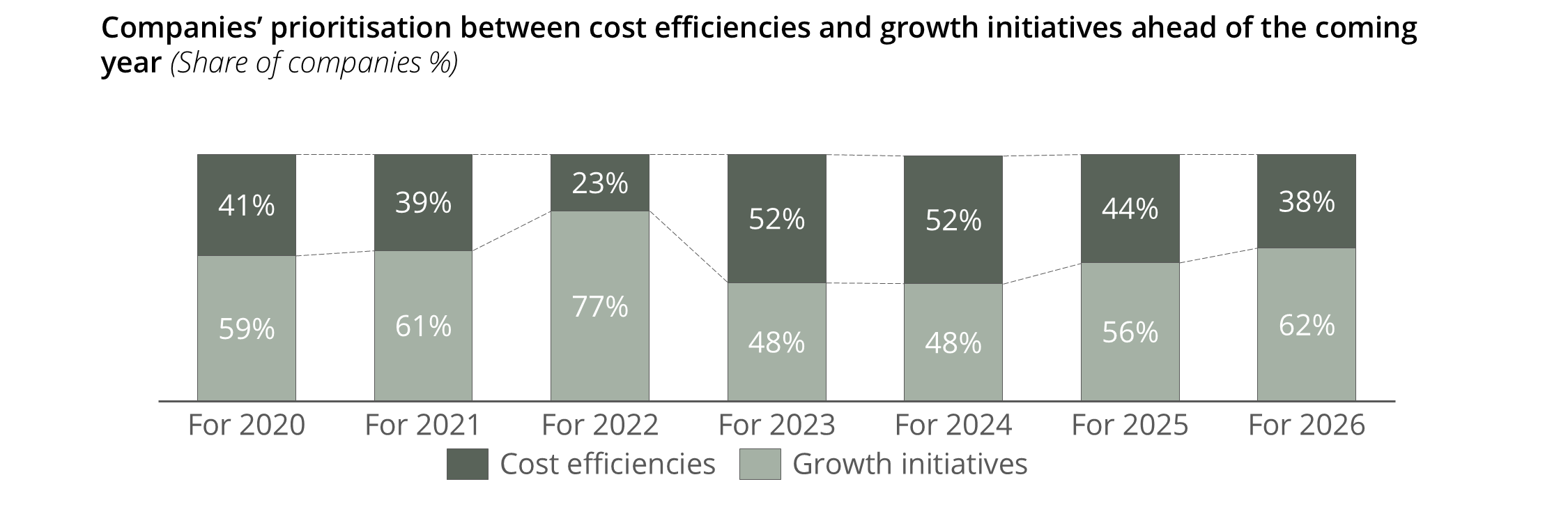

Growth focus strengthens ahead of 2026, more companies prioritise growth initiatives and fewer prioritise cost efficiencies, but cyclical industries remain more focused on efficiency

Just over half of respondents prioritise growth initiatives over cost efficiencies ahead of 2026…

> The trend from last year continues and ahead of 2026 even more companies are prioritising growth initiatives while fewer are focusing on cost efficiencies.

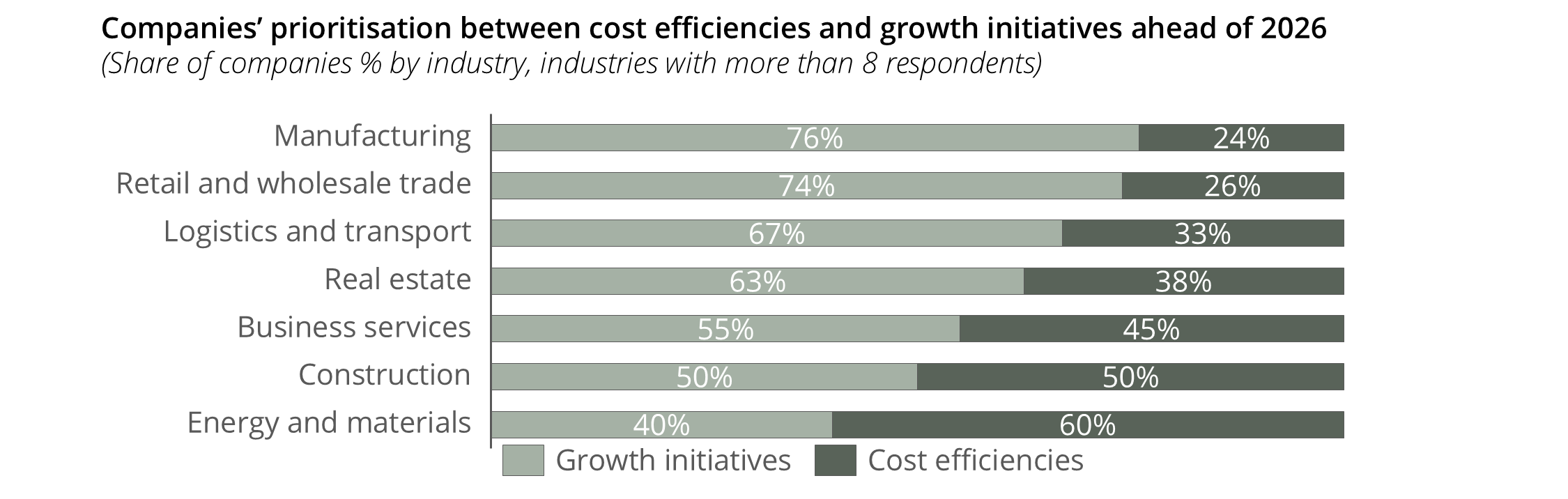

…but it varies across industries.

> Chief executives in manufacturing and in retail and wholesale will prioritise growth initiatives over cost efficiencies, which can be explained by a belief that investment willingness among both consumers and companies will increase.

> Construction and energy stand out for a greater focus on cost efficiencies, which can be linked to these industries being more affected by economic swings and recent years’ high interest rates.

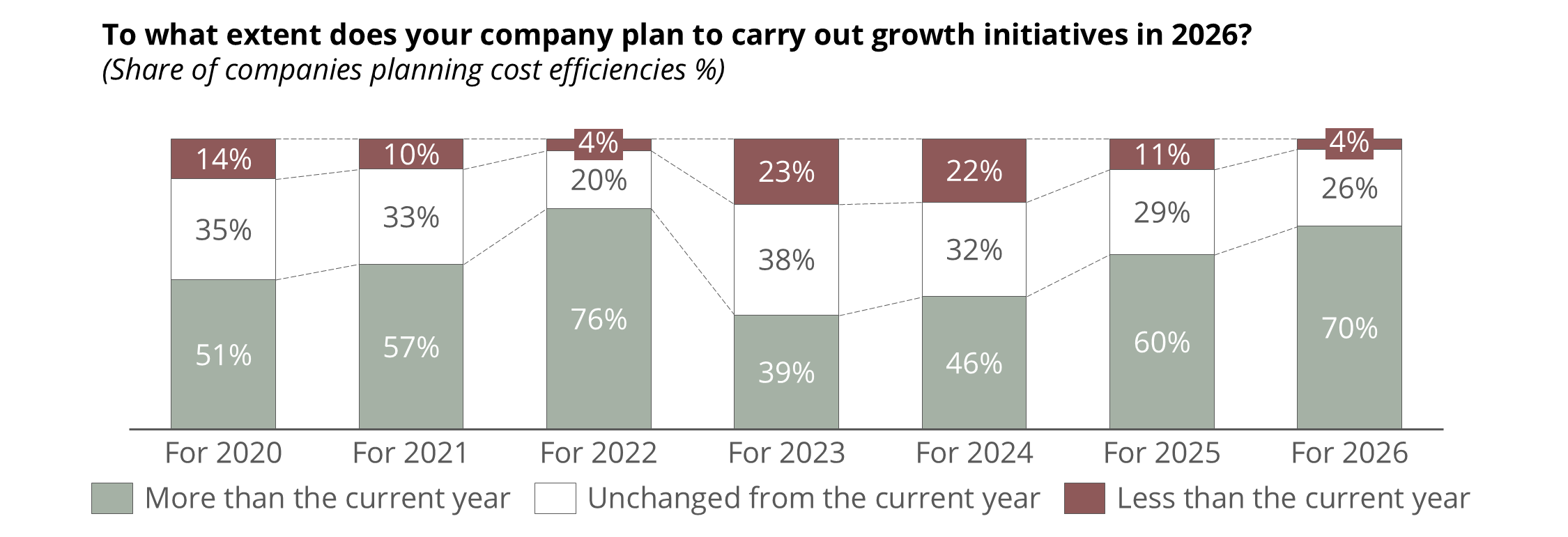

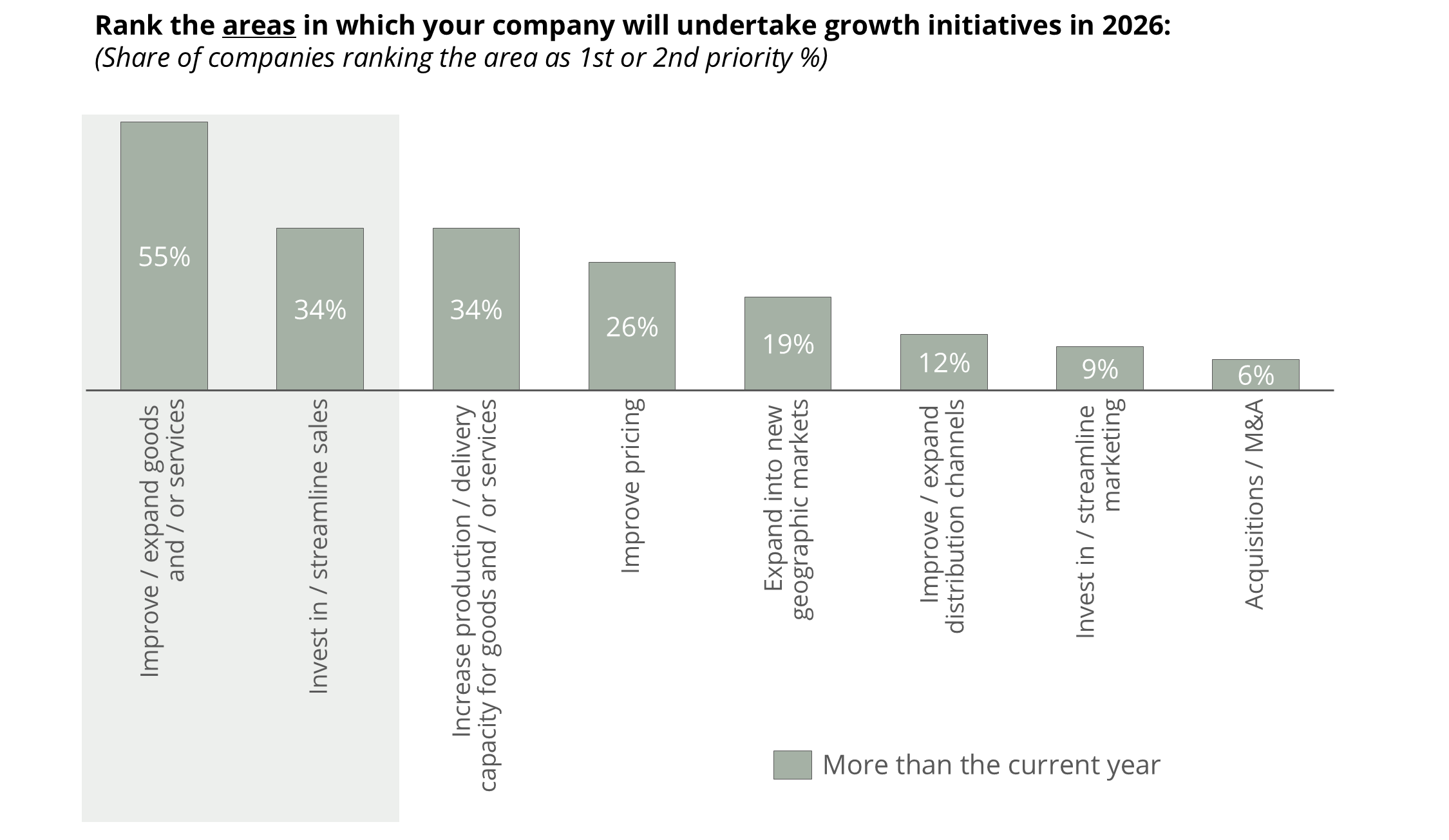

Companies show increased optimism ahead of 2026 and plan more growth initiatives than in previous years, focusing on developing goods and services, capacity increases and sales

70% of companies plan to invest more in growth compared with current levels, a continued increase from the previous year’s plans…

…and the focus will be on improvement and innovation, with companies prioritising the development of goods and services and sales ahead of 2026.

> A majority of companies (55%) plan to improve or expand their goods and services, suggesting growth will mainly be driven by developing and broadening the offer – through both product development and expanded/repackaged services.

> Investments in sales and production capacity are also ranked highly, reflecting a need to strengthen both revenue generation and delivery capability.

> Despite the growth focus, M&A is low priority (6%), suggesting companies want to drive growth organically rather than through acquisitions.

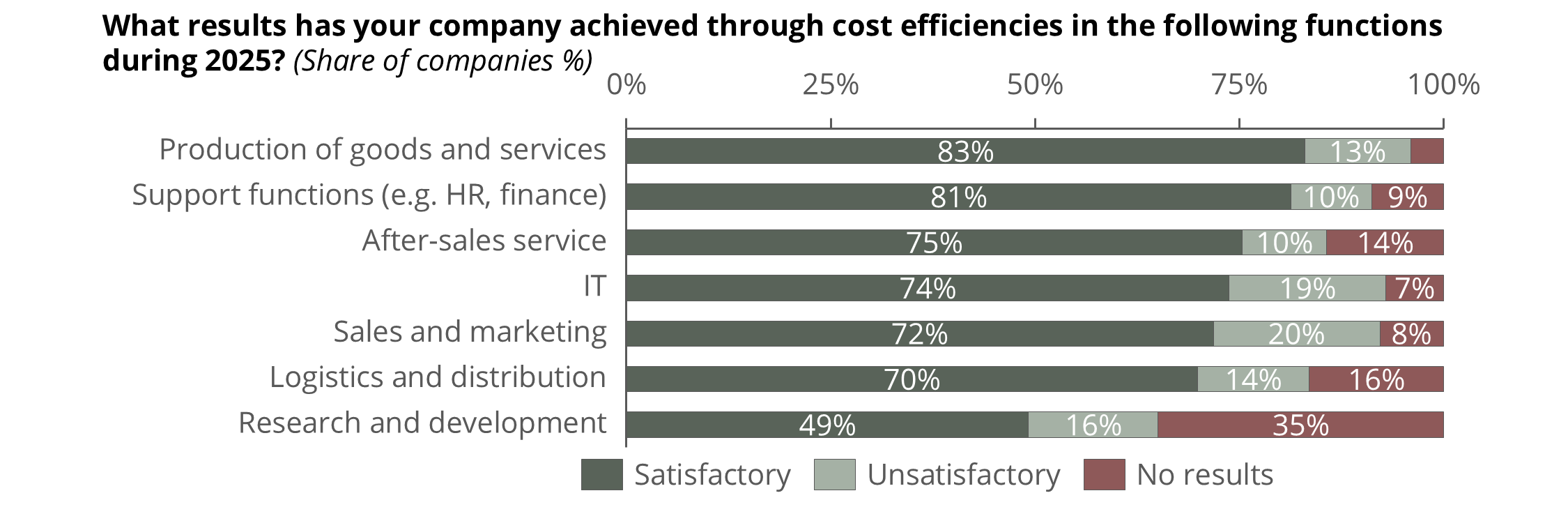

Growth as the main focus in 2026 is likely driven by chief executives seeing a satisfactory effect from cost efficiencies in 2025

Most cost-efficiency measures in 2025 have been satisfactory, with production-related measures once again delivering the best results…

> Efficiency work has produced the most positive outcomes where measures are most operational and measurable (production and support functions), while research and development stands out for lower precision and more respondents not seeing results.

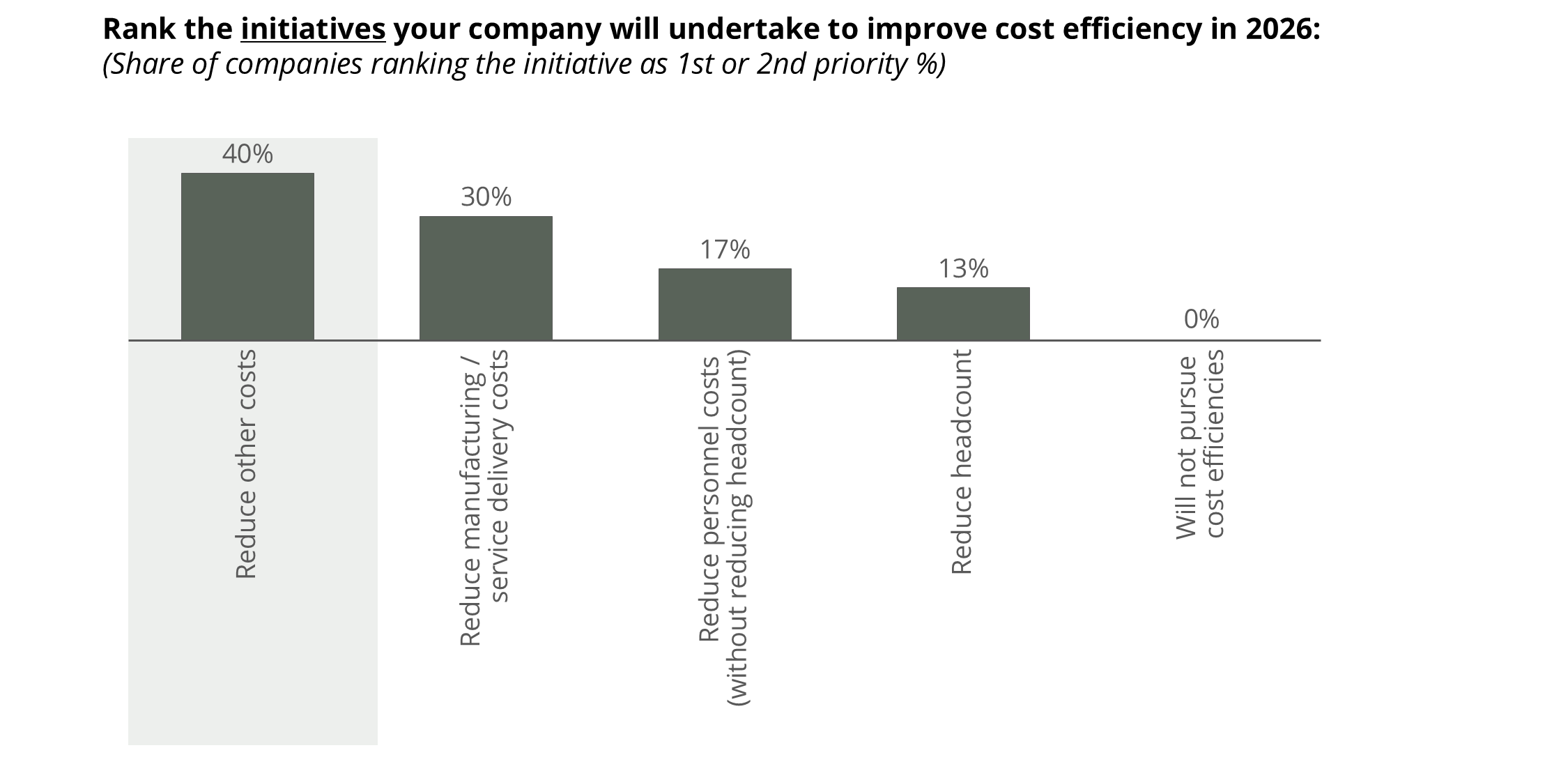

…and in 2026 companies plan to drive efficiencies mainly through reduced other costs and efficiency improvements in the supplier and manufacturing chain.

> The study shows that cost efficiencies are mainly about reducing other costs and streamlining the supplier and manufacturing chain, rather than reducing headcount.

”Streamline services that are not directly linked to sales or product creation to reduce overhead.”

Tobias Moberg, Moberg Bil

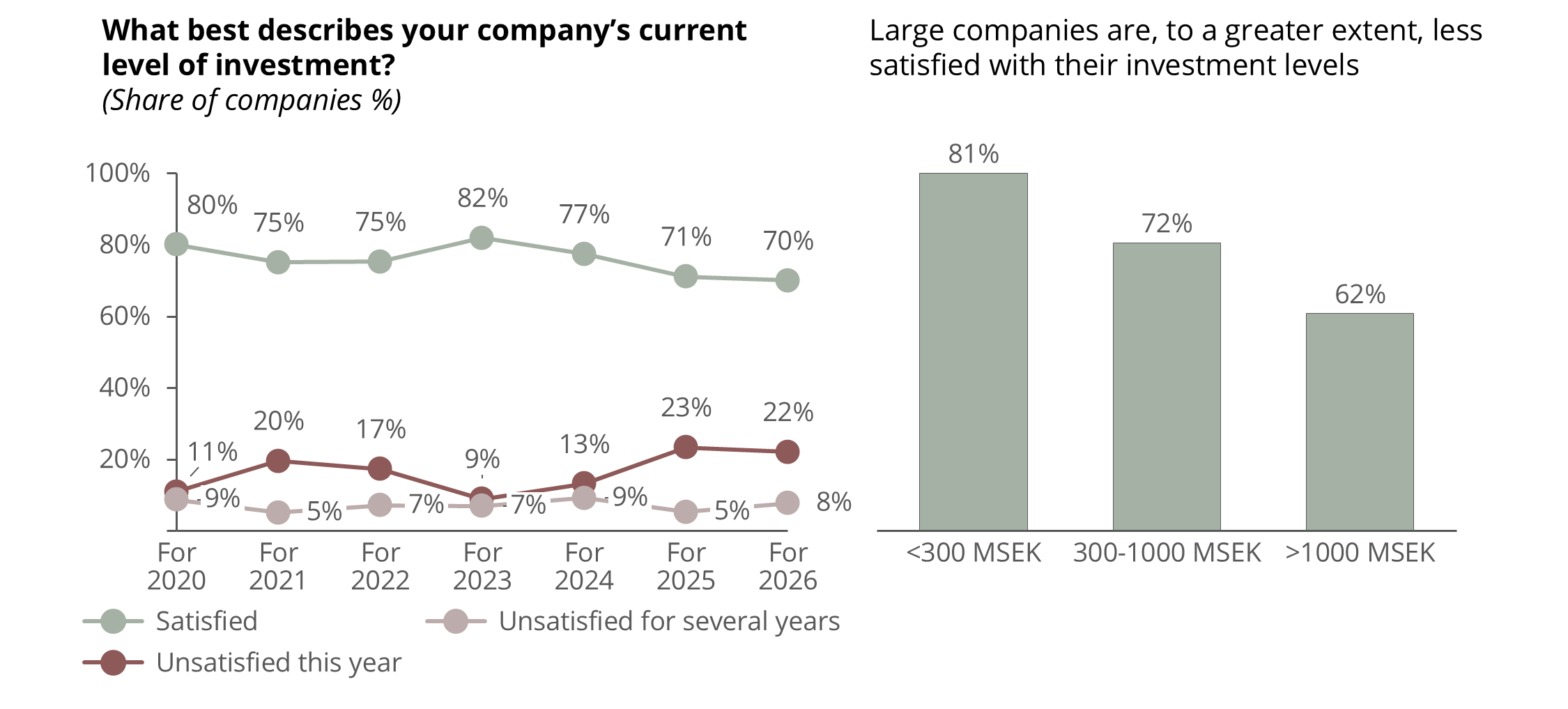

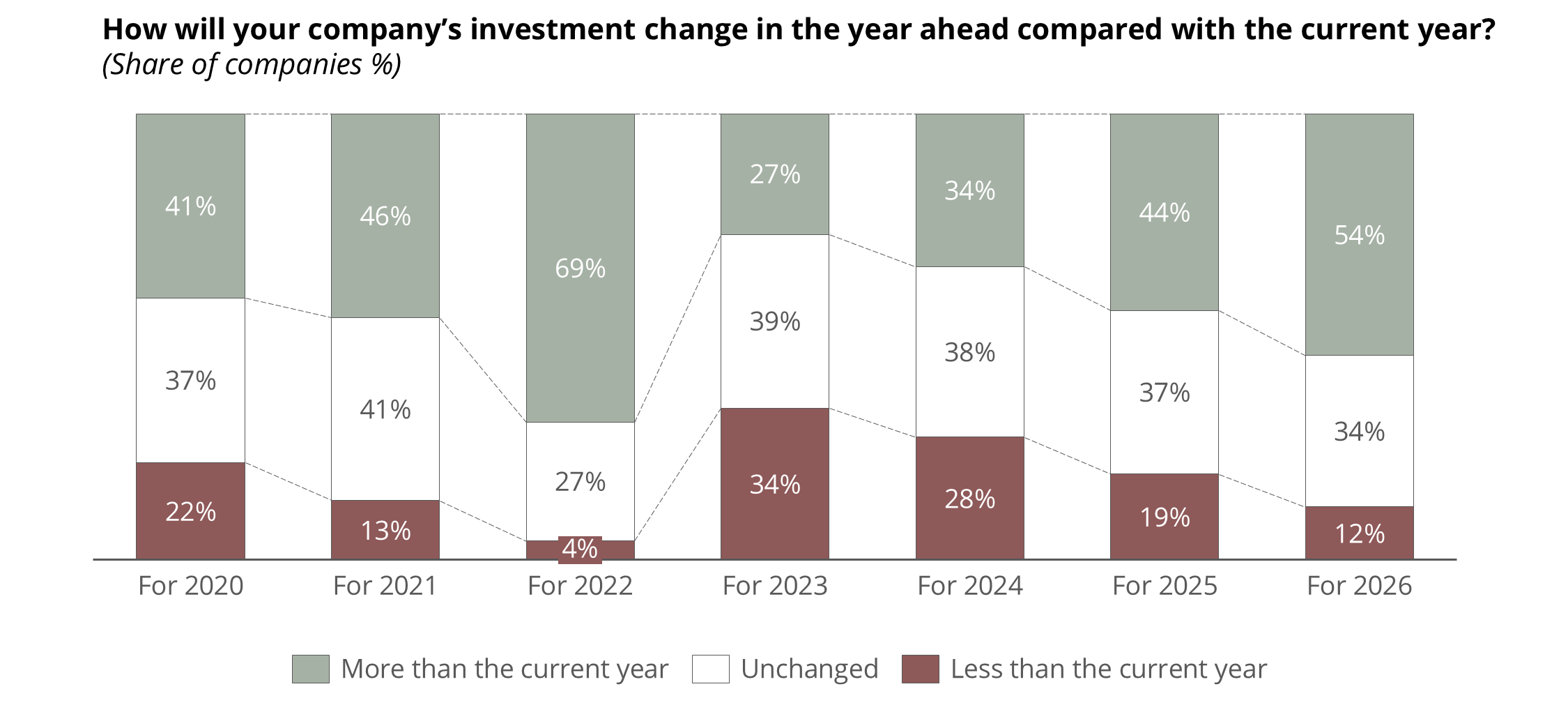

More companies are stepping up investment ahead of 2026, a potential consequence of limited opportunities to carry out investments over the past two years

A record-low share of respondents say they were able to carry out desired investments during 2025 (70%)…

…but it is clear that companies plan to invest more in 2026 than was planned ahead of 2025.

> The share of chief executives planning to invest more than current levels has increased further ahead of 2026, signalling that the recovery in investment appetite is continuing.

> Since 2023, the share of chief executives planning to invest more than the current year has risen steadily – from 27% to 54%, corresponding to an average increase of around 26% per year (relative).

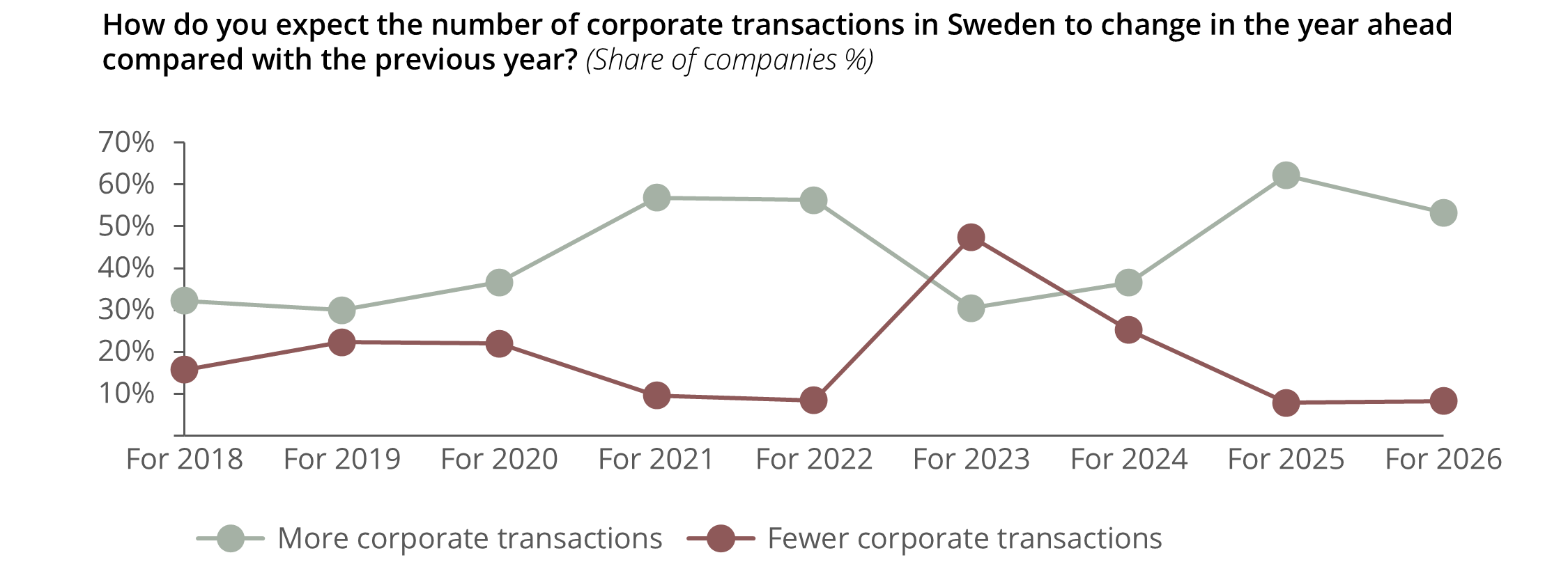

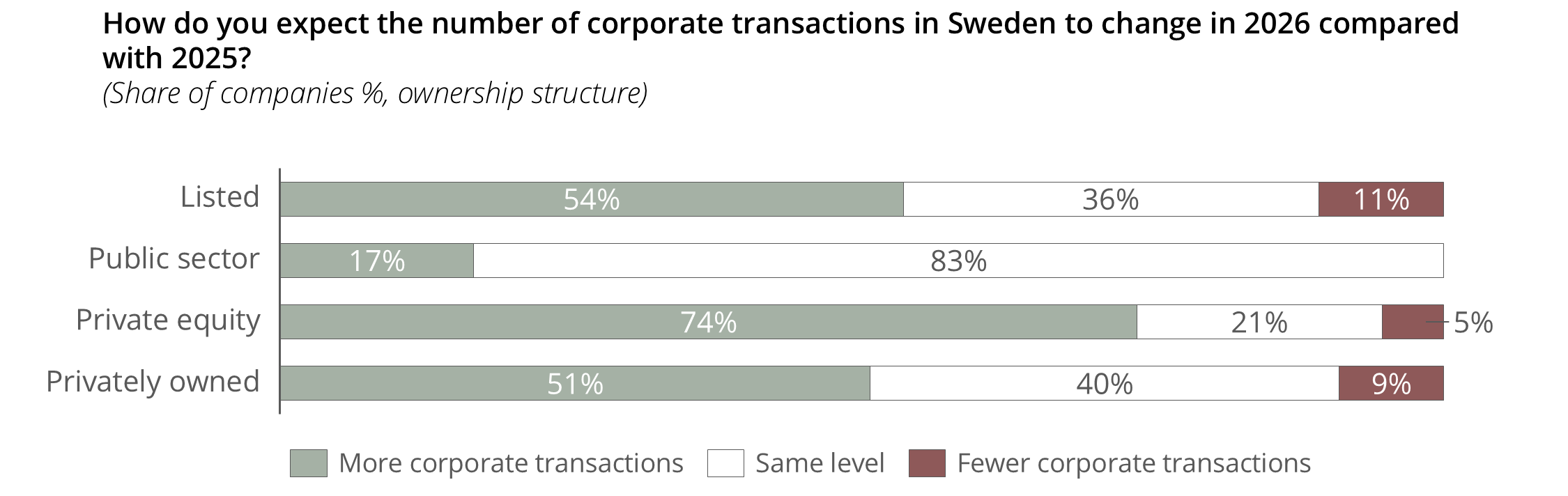

Despite M&A not being ranked as a focus area for growth, expectations of more corporate transactions in the market generally remain strong ahead of 2026, particularly among private equity-owned companies

The number of Swedish chief executives who foresee more acquisitions and divestments of businesses in Sweden remains high…

> Expectations for corporate transactions remain high (53%) and above a normal year, but below last year’s peak.

…with the strongest optimism among private equity-owned companies.

> Private equity-owned companies are the most optimistic, with the highest share expecting more deals and the lowest share expecting fewer, reflecting a high propensity to transact in this ownership form.

> An overwhelming majority (89%) of business leaders at listed companies expect the number of corporate transactions in 2026 to be maintained or increase, indicating cautious optimism in this sector

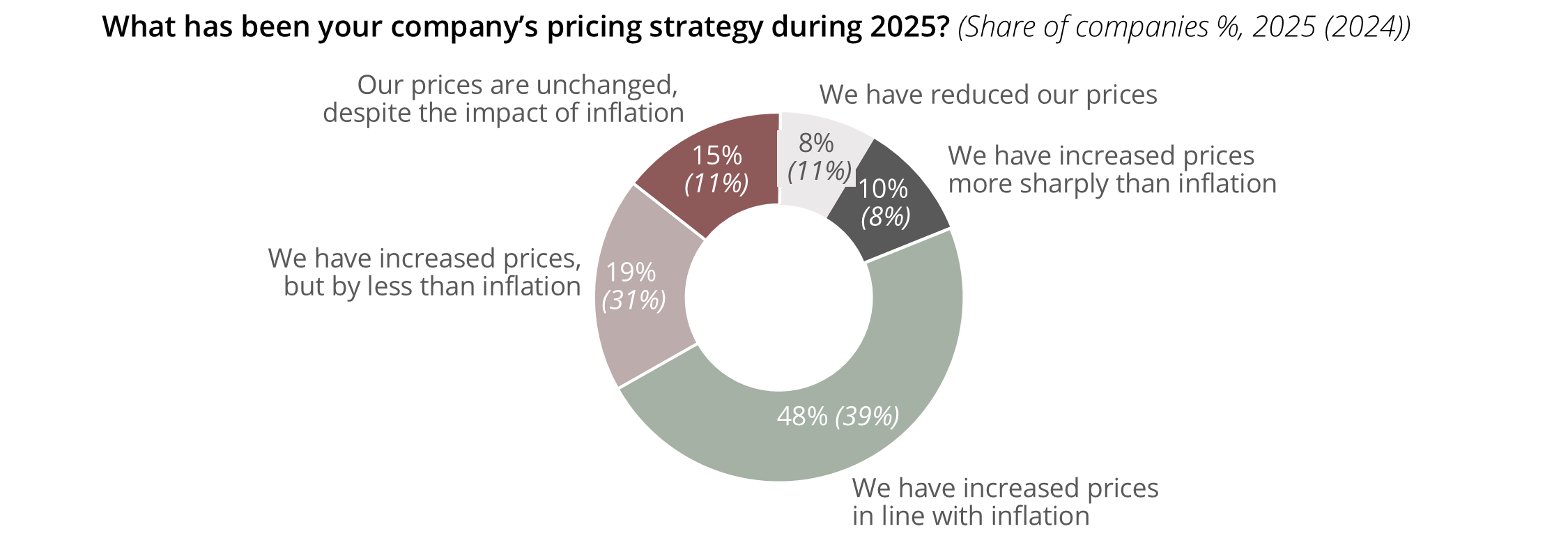

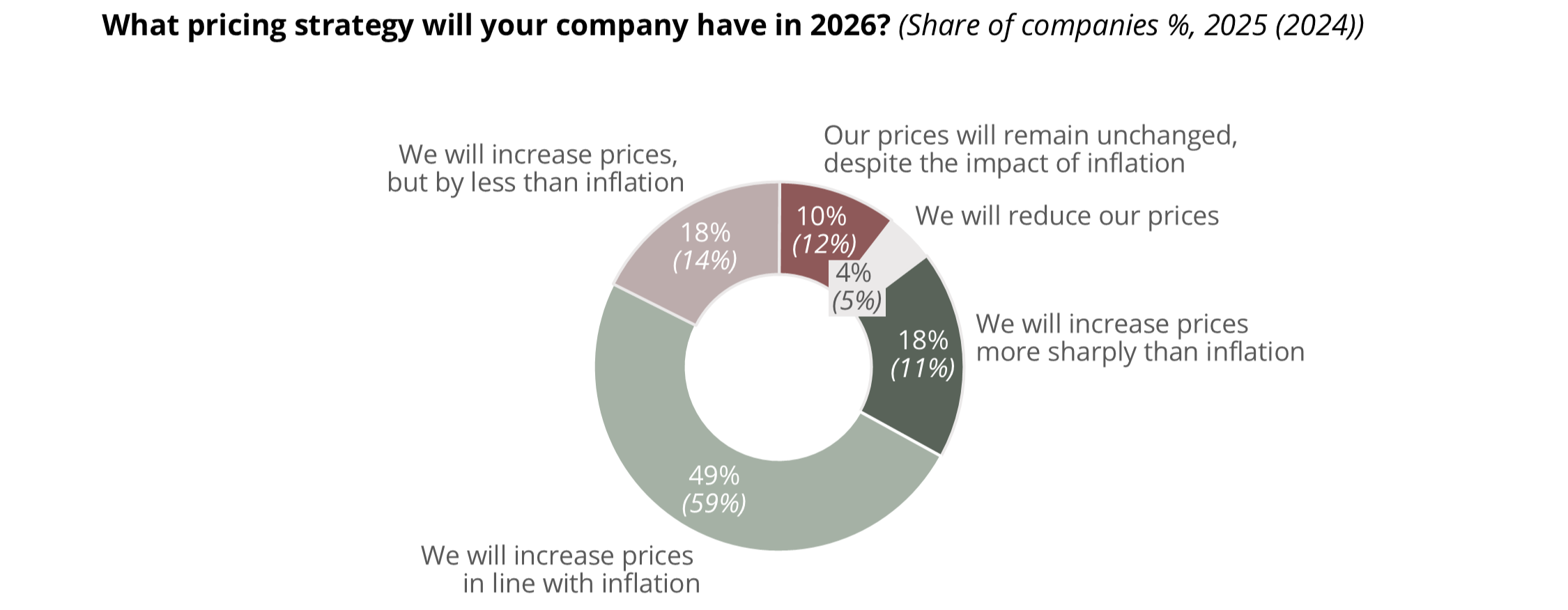

More chief executives are planning price increases than in 2025 (78% versus 70% last year), and 18% expect to raise prices more than inflation in 2026

58% of respondents have already adjusted their prices in line with or above inflation during 2025…

> Ahead of 2025, almost 70% of companies planned to raise prices in line with or above inflation, but the outcome was lower – 58% did so. The outcome suggests more cautious pricing than planned.

…and around 67% of respondents plan to raise their prices in line with or above inflation during 2026.

AI

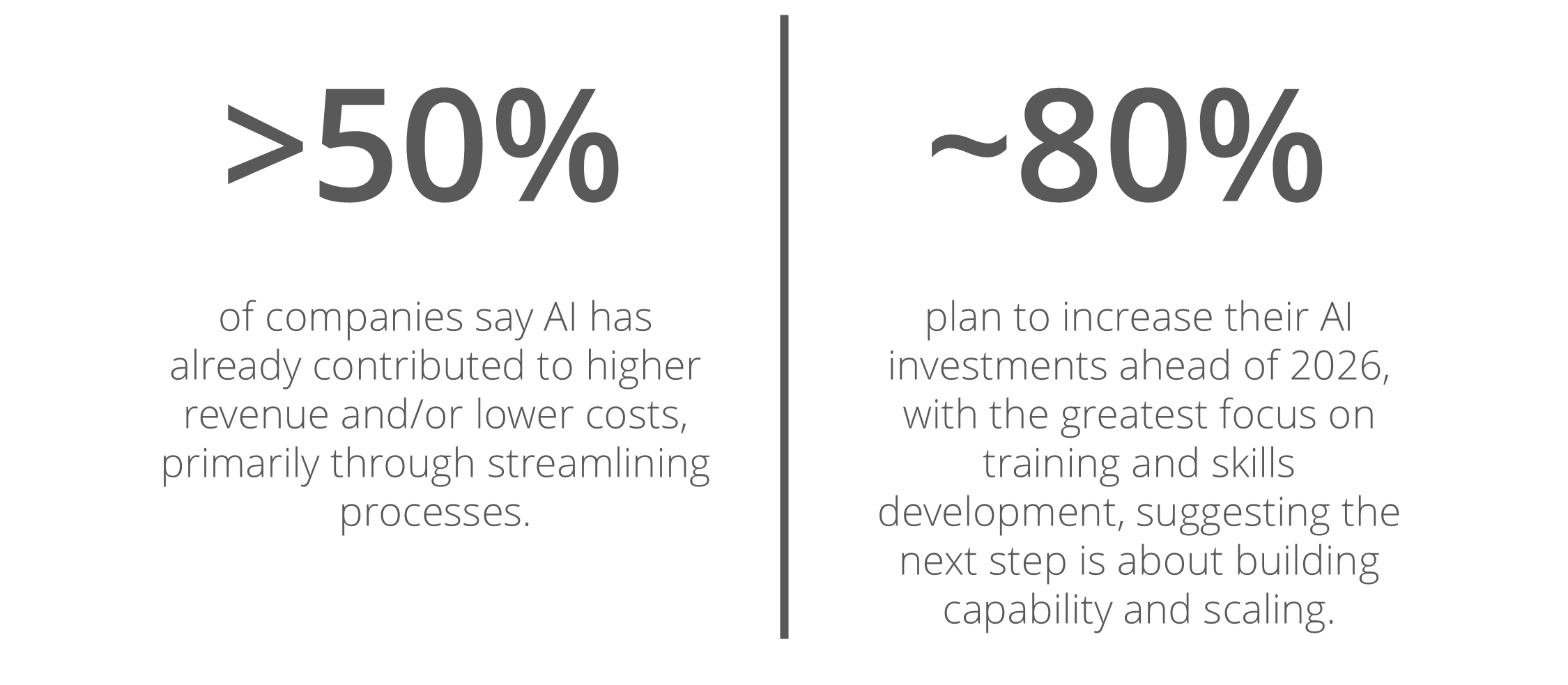

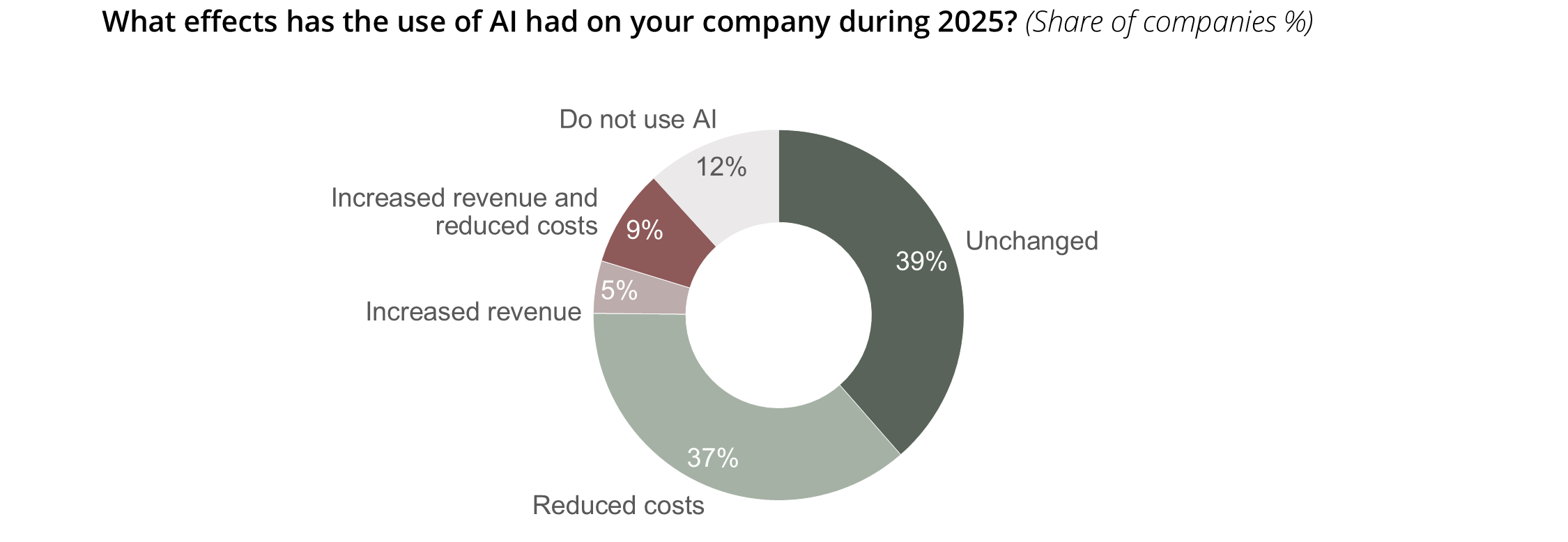

A growing number of companies are seeing positive effects from AI, primarily lower costs, but also in the form of higher revenue

51% of respondents have experienced positive effects from AI during 2025, such as higher revenue and/or lower costs…

> The share of companies that say they do not use AI has fallen from 36% to 12%, suggesting AI usage has increased markedly since the previous year.

”AI is used primarily to improve the quality of tasks, streamline processes and free up time for other tasks among employees.”

CEO, Retail and wholesale

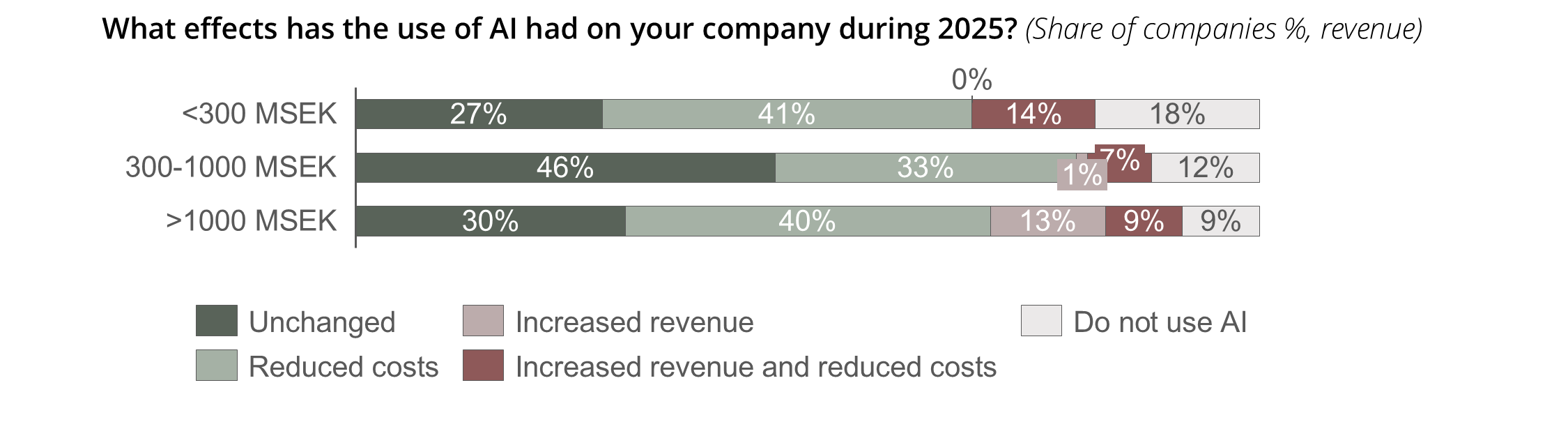

…primarily in the form of reduced costs, while larger companies more often see revenue effects and smaller companies more often do not use AI.

> Reduced costs are the clearest effect across all size categories, suggesting AI is mainly used for efficiency or automation rather than to drive revenue in the short term.

> Larger companies (>1000 MSEK) more often see revenue effects than smaller companies, which may indicate they have come further in scaling AI in customer-facing processes.

> Smaller companies (<300 MSEK) have the highest share not using AI, which may reflect resource and competence gaps, or that the benefits are harder to realise, or limited access to relevant data.

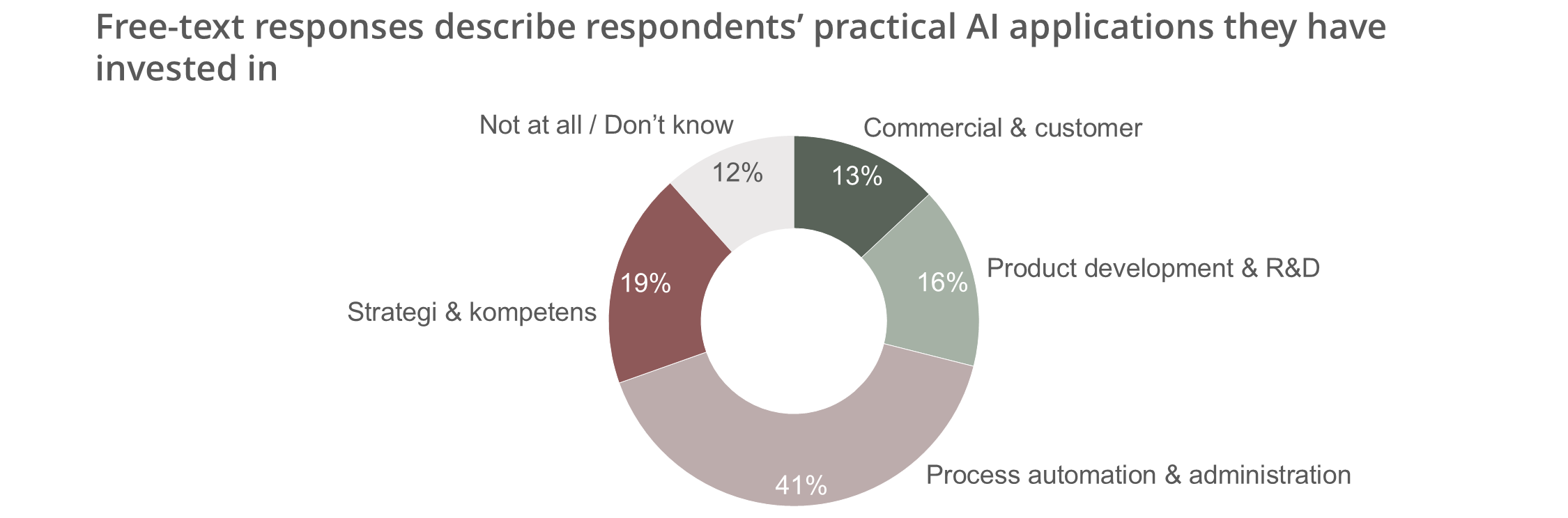

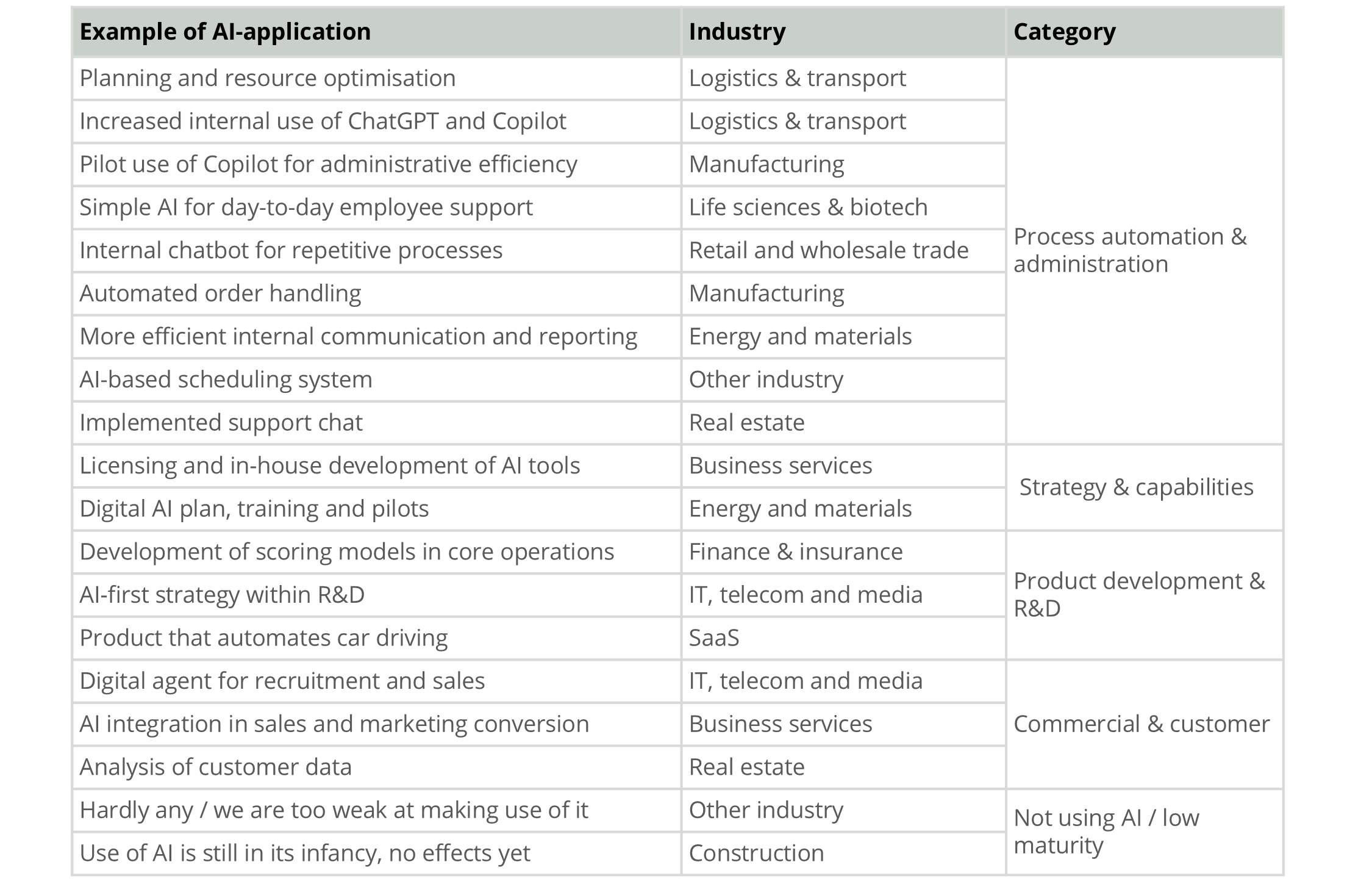

Practical AI applications have not changed radically between 2024 and 2025, with process automation and administration most common. Core operations and commercial use cases are increasingly in focus

> Asked about practical AI applications companies invested in during 2025, we see that process automation & Admin dominates broadly across industries; product development & R&D is most evident in IT/telecom/media, SaaS and finance, while strategy and competence are most visible in industrial and energy companies.

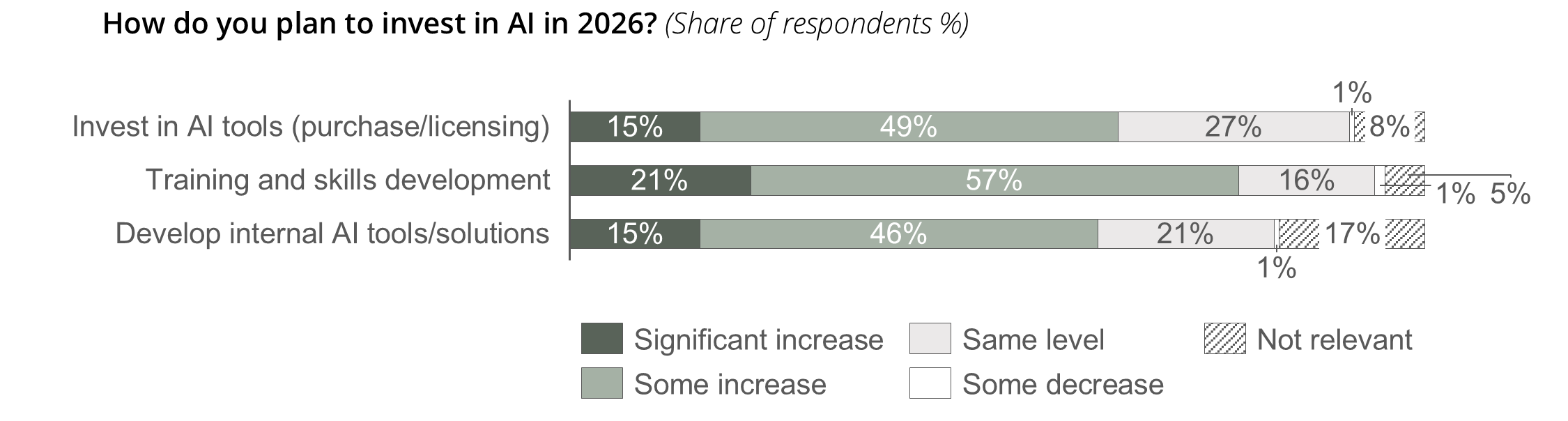

Over half of chief executives plan to increase their AI investments during 2026 with a focus on competence and tools, where time and organisational capacity are a decisive prerequisite

Most of the surveyed companies plan to increase their AI investments during 2026…

> A clear majority of companies plan to increase their AI investments in the coming year, with a particular focus on training and skills development.

> Only around 1% say they expect a reduction in any area – showing that AI is now an established and long-term part of companies’ business development.

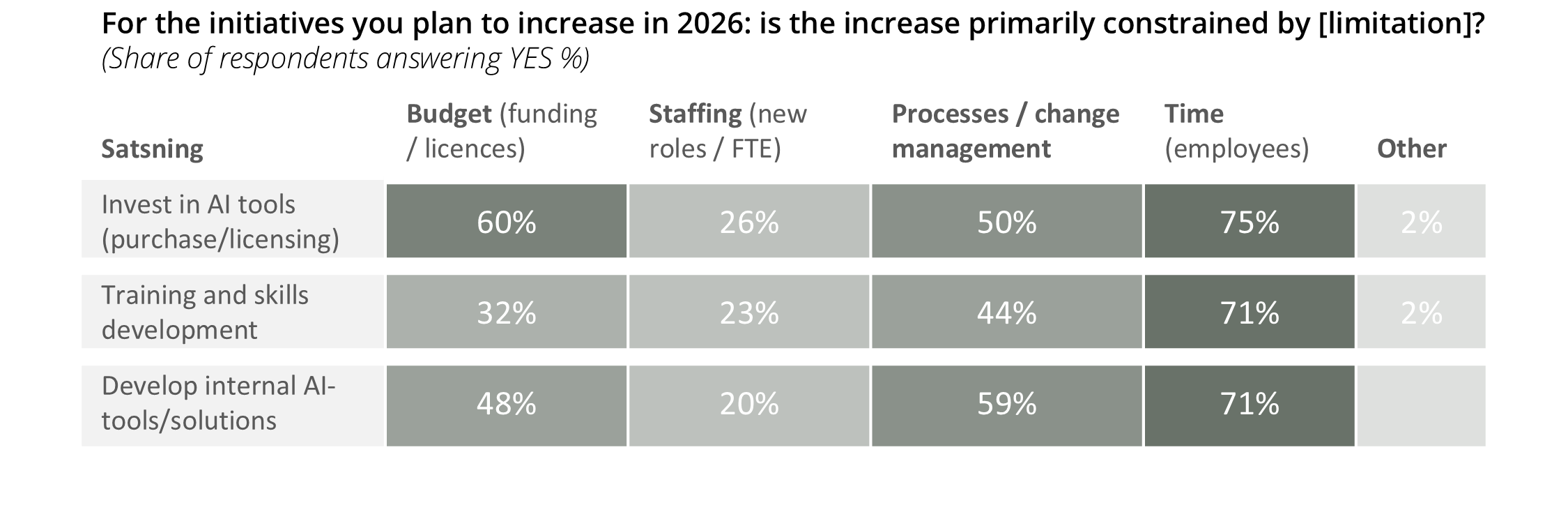

…where the most important prerequisite is time and organisational capacity, rather than the technology itself.

> Time is the greatest constraint across all investment areas, indicating that scaling AI is mainly about organisational capacity rather than just technology.

> Internal development requires more change management (59%) than new AI tools (50%), while purchasing AI tools is more often driven by budget (60%), suggesting that “build” is a larger transformation, and “buy” more an investment question.

US Tariffs

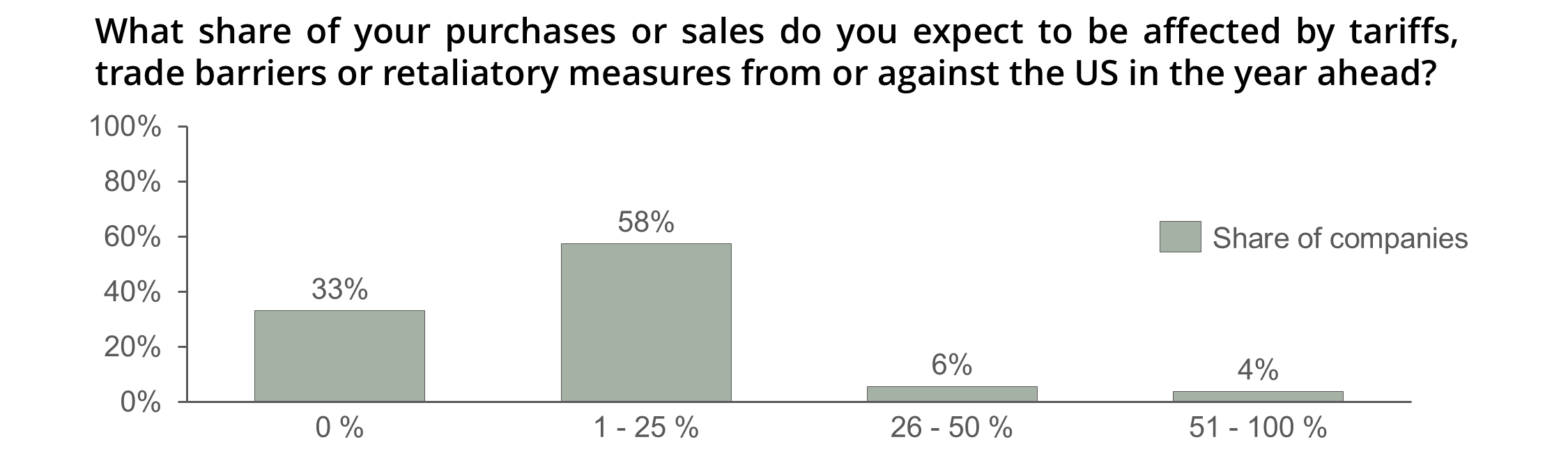

Most respondents judge the effect of US tariffs to be manageable, even though it may differ between industries – trade and industry are most exposed

> For the majority (1–25%), tariff risk is often about margin friction and operational complexity rather than significant transformation. The impact of exposure can, however, be large if it is directed at a critical flow (a key component, a major customer or a limited supplier base).

> For the group with >25% exposure, the conclusion is different. That group needs to take more measures than general risk actions. Tariffs are expected to hit these companies’ pricing model, contracts and supplier set-up directly, as well as their customer relationships.

Industries with the highest exposure (share of companies with >25% exposure):

- Retail and wholesale: around 16% are above 25% (3 of 19).

- Manufacturing and Energy, raw materials and materials: around 10% above 25% (3 of 29 in each group).

This is logical in a tariff context: trade and industry more often have direct goods flows, component dependencies or export flows where tariffs quickly become both a cost and a demand issue.

”The great concern around US tariffs is largely overblown, and in Europe we have reached an agreement with the US that most companies seem able to live with… many companies seem to believe tariffs can be managed both by steering production flows and making necessary price adjustments to compensate for tariff-driven cost increases.”

Johan Javeus, Chief Strategist SEB

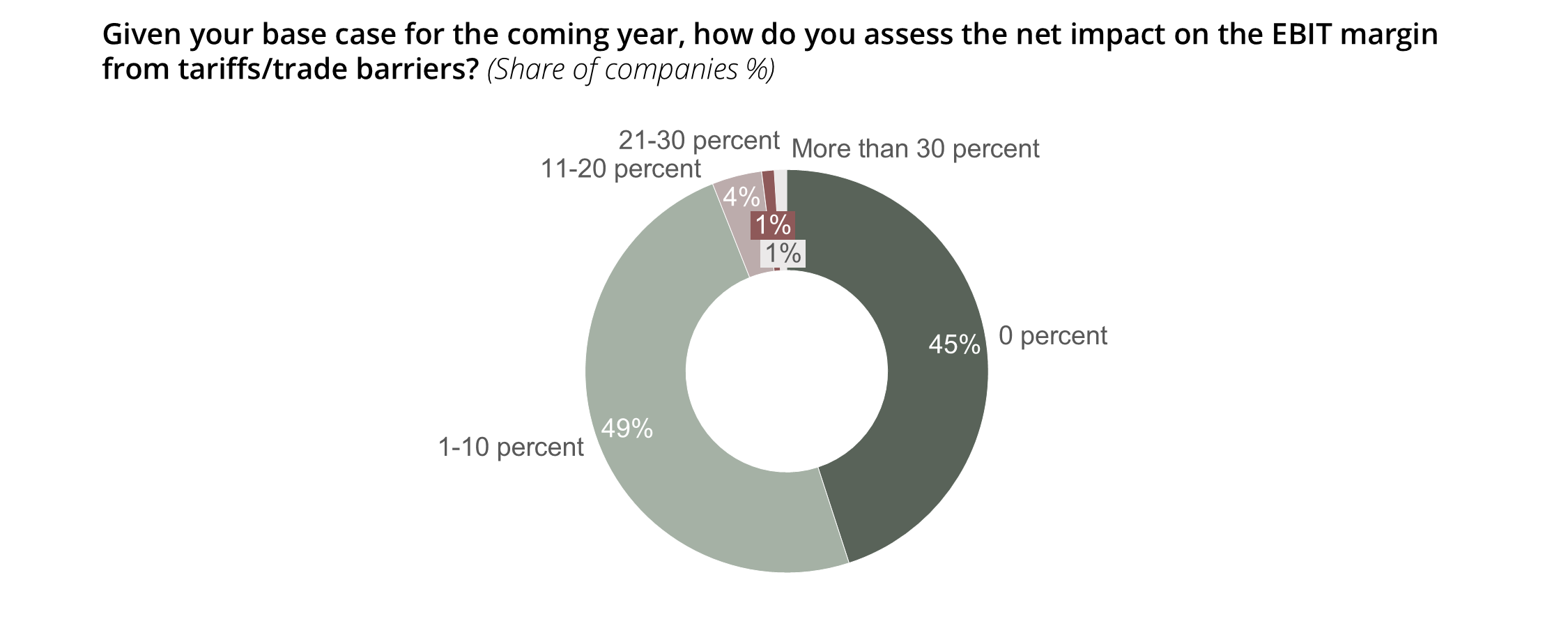

The EBIT impact is also judged manageable: 45% expect a 0% net effect even though 33% say they have no exposure at all

A large share of companies expect to be able to offset the effect through pricing, mix, procurement and internal programmes…

Respondents’ answers show that there is no direct correlation between exposure to US tariffs and the impact on EBIT.

Among companies with >25% US exposure, several still only see a 0–10% EBIT effect. This suggests they expect to be able to offset tariffs, for example through:

- price increases to customers,

- built-in contract mechanisms (indexation, cost pass-through),

- or restructuring flows and suppliers.

…at the same time, the data show that not everyone believes they can neutralise the impact – almost half of companies expect a 1–10% margin decline and 4% expect an EBIT effect of over 10%.

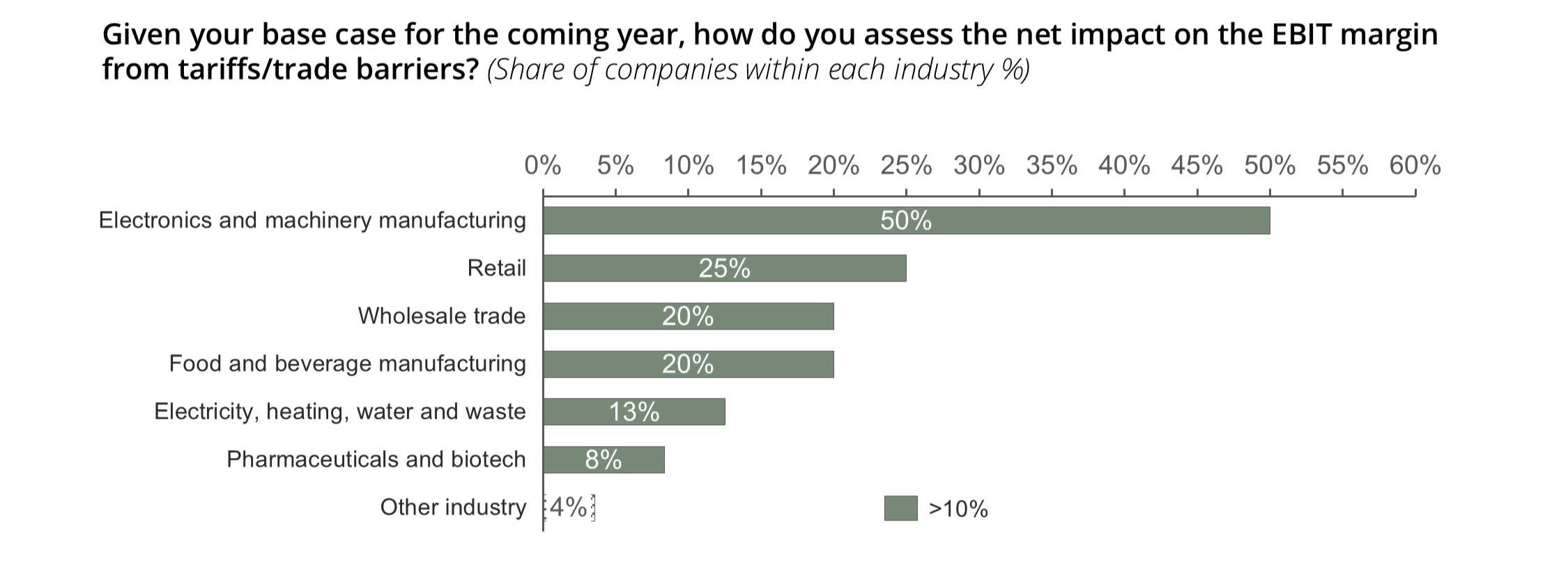

Industries that stand out for EBIT pressure (>10% EBIT effect):

- Manufacturing industries

- Trading companies

- Energy, raw materials and materials

Agenda 2026

The 2026 chief executive agenda centres on profitable growth, making digitalisation and AI deliver a positive EBIT, and building the skills and sustainability capabilities needed for the next wave of regulation and customer demands

Reflections

In this chapter, we highlight selected perspectives from this year’s CEO Study.

Based on CEO Study 2026, we summarise four perspectives on how Swedish CEOs view market developments, strategic shifts and new normals ahead of 2026. These perspectives draw exclusively on the study’s results and offer an overall picture of how chief executives interpret the external environment and their strategic choices.

Are Swedish companies ready for 2026?

From optimism to an executable growth strategy

This year’s VD Study points to a clear shift: more business leaders are entering 2026 with a more offensive agenda in which growth is prioritised ahead of cost focus. At the same time, we see a market where the recovery is driven by improved conditions – but also by increased uncertainty linked to geopolitics and trade barriers.

In such a market, a growth strategy becomes less an ambition and more a portfolio of choices: where we should win, how we should win, and which initiatives actually move revenue and profitability.

At Axholmen, we work together with leadership teams to take strategy from ambition to a prioritised execution plan, with clear commercial levers and measurable impact.

What should companies consider when formulating their growth strategy?

> Sharpen “Where & How we will win”: Combine customer and market insights with internal quantitative data to eliminate guesswork and clearly choose segments, offers and channels based on fact-based insights where you have the greatest likelihood of winning, and define what is required to do so.

> Build a commercial growth engine – not a list of initiatives: Translate the strategy into a coherent commercial model (value proposition, packaging, sales logic, pricing, delivery) so that each activity reinforces the next.

> Prioritise and link to impact: Set a clear prioritisation logic around customer segments, markets, channels, etc. and follow up in a way that makes it easy to scale what works and stop what does not deliver results.

> Secure execution capability: In a more capacity-constrained reality, resource allocation and the governance model become decisive. Establish ownership, decision points and a plan that holds even when the market turns.

Pricing as profitable growth – in a more differentiated market

After several years of inflation and cost pressure, pricing remains one of the most powerful tools to defend and develop margins – but in 2026 it is less about broad price rises and more about precision.

In the VD Study, 58% state that during 2025 they have already adjusted prices in line with or above inflation. Ahead of 2026, around 67% plan to do the same – and at the same time 78% plan to implement price increases, of which 18% state they will raise more than inflation.

At the same time, the study points to a shift in which AI and data-driven ways of working are highlighted as tools to make better decisions and standardise ways of working in commercial processes. For pricing, this means an opportunity to move from “price adjustment” to a pricing model that links price to customer value, cost drivers and actual willingness to pay.

With new uncertainties (e.g. trade barriers), pricing and commercial terms also become part of a company’s resilience. For many companies, pricing is therefore both a profitability issue and a governance issue ahead of 2026.

What should companies consider ahead of 2026 in relation to pricing?

> Move from price adjustment to pricing strategy: Establish a clear logic for when and how prices change (governance, mandate, process, communication) so that price becomes a steering instrument, not an ad hoc reaction.

> Differentiate by value and customer economics: Segment customers based on value, behaviour and cost-to-serve, and build a structure that enables targeted measures—from price negotiations to value-creating add-on services.

> Secure pricing through change (e.g. M&A, new offerings): Harmonisation, packaging and terms must align to avoid leakage in net price and create clarity in the customer interface.

> Use data and AI where it actually makes a difference: Prioritise use cases that strengthen day-to-day pricing decisions (e.g. pricing by segment/product, deviation handling, quotation logic) and build organisational buy-in.

Concretizing a growth strategy

For business-to-business companies with the ambition to grow, a growth strategy is usually developed based on a point-of-departure analysis combined with customer and market insights. However, to make the plan successful, actions need to be concretely defined and planned. Without converting a theoretical strategy into doable actions, limited positive effects can be expected.

Read more

Pricing – Your company’s untapped source of profit potential?

Did you know that pricing is the profit lever that both generate the largest and quickest bottom-line impact?

Despite its large potential, most companies are not actively working with pricing. Instead, many companies focus on cost reductions and sales volume increase initiatives, where the financial benefits are significantly lower.

Read more

Cost reduction – concrete tips to maximize results

Costs that have increased over time relative to revenues, new market conditions or the need to release capital? There are many drivers to reduce a company’s costs. Whatever the reason and the inherent potential for the company, implementing a cost reduction program is usually associated with challenges.

Read more

Maximise revenues in a profitable way

How can you maximise your company’s revenue in a profitable way? We help you analyze and implement prioritized initiatives. It’s about offering the right product, through the right channel, at a price that optimizes long-term profitability.

Increase profitability through increased efficiency

How do you maintain your company’s competitiveness in a world that’s constantly changing? We help you improve commercial efficiency throughout the transformation journey. In practice, it’s about identifying, prioritizing, and executing the activities expected to deliver the greatest results.

20 years experience from B2B and B2C Commercial Excellence projects within Manufacturing, Logistics, Transport, Enterprise and Consumer SW/HW, Professional Services, Managed Services, Financial Services and Consumer Goods.

Milosz Tersmeden, Partner and CEO

+46 76 161 21 99

25 years of experience both as a consultant and in line roles, delivering results on both the top and bottom line through commercial optimization, offering design and pricing, strategic transformations, structurally redesigned operating models, sourcing and outsourcing, organizational design and sizing, and working capital optimization across multiple industries.

Erik Mokvist, Partner

+46 70 749 14 95

15 years’ experience of successfully helping clients deliver realised improvements in profitability, on both the revenue and cost sides. Has led 20+ Commercial Excellence projects, with a focus on pricing strategy, price optimisation, revenue assurance and sales leadership.

Richard Cecchini, Partner

+46 73 068 11 34

Specialist in commercial strategy, supporting companies across areas including marketing, pricing and sales, and author of five books on improving corporate pricing and profitability.

Felix Mörée, Partner

+46 70 332 45 29

15 years’ consulting experience, with assignments spanning Operational Excellence, Lean, modularisation and customer-oriented organisations and value streams, across both product-based companies and service businesses.

Gustaf Smedman, Partner

+46 70 730 79 94

15 years’ consulting experience spanning strategy, operational efficiency, spend reduction, operating model revisions, organizational redesign and turnaround projects. Has supported large and medium-sized companies across manufacturing, retail, construction, energy & utilities, transportation and telecom.

Daniel Bajka, Partner

+46 73 057 51 90

About Axholmen

Since our founding in 2007, we have helped companies improve their profitability. From the outset, our ambition was clear: to deliver a modern alternative to the global management consultancies. We address critical business challenges with the aim of increasing profitability.

Simpler and more results-focused

Axholmen was founded on the idea of creating a simpler, more results-driven way of delivering management consulting services.

Sustainable and tangible results

Our philosophy is that consulting assignments should deliver sustainable and tangible results. That is why we are prepared to share commercial risk and link our fees to the value we create together with our clients.

Improved profitability

Our core offering is to solve critical business challenges in order to improve profitability. We have experience across most industries.

Driven and business-focused

We are uncompromising in our recruitment. All our management consultants are hand-picked for their expertise, drive and genuine business focus.

Feel free to contact us for more information or to schedule a no-obligation meeting