WHAT IS INDIRECT PROCUREMENT?

Indirect procurement is the acquisition of goods and services not used as input to the production of the goods or services the company is selling.

In contrast to direct procurement, indirect is not typically related to a company’s core business, nor does it include personnel costs. Which cost categories are included can vary depending on the business, but typically include office supplies, marketing, IT, consultants, logistics, travel, and facility management.

INCREASE PROFITABILITY, MINIMIZE PAIN

New profitability targets, cost-cutting packages, and cutbacks are announced daily in the business press. How and where to find these cost savings are major issues for many companies.

Increasing profitability with limited impact on a company’s day-to-day operations can often be achieved through measures within indirect cost categories as they do not concern staff or the products/services the company is selling. In some cases, it may even be sufficient to review these costs and avoid staff reductions in order to achieve savings targets.

Many Swedish companies have been working on staff efficiency for several years. Consequently, further staff reductions have low potential and carry a high risk. Complementary work to reduce indirect purchasing costs is therefore often a wise idea.

UNTAPPED POTENTIAL

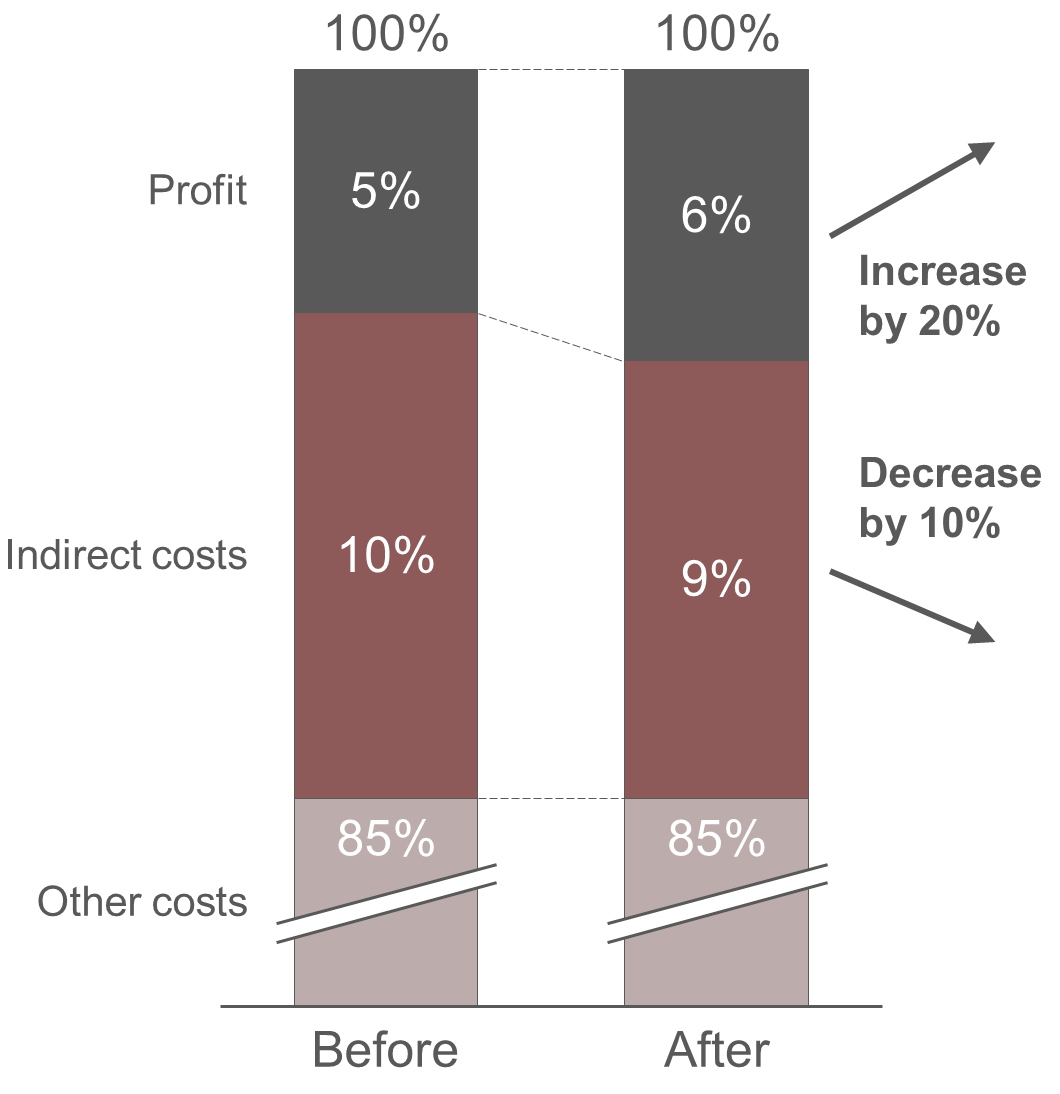

Indirect costs often represent a significant proportion of companies’ total cost, typically between 5-15% of turnover. Therefore, a cost reduction has a significant impact on the company’s profits, see the example in Figure 1 above.

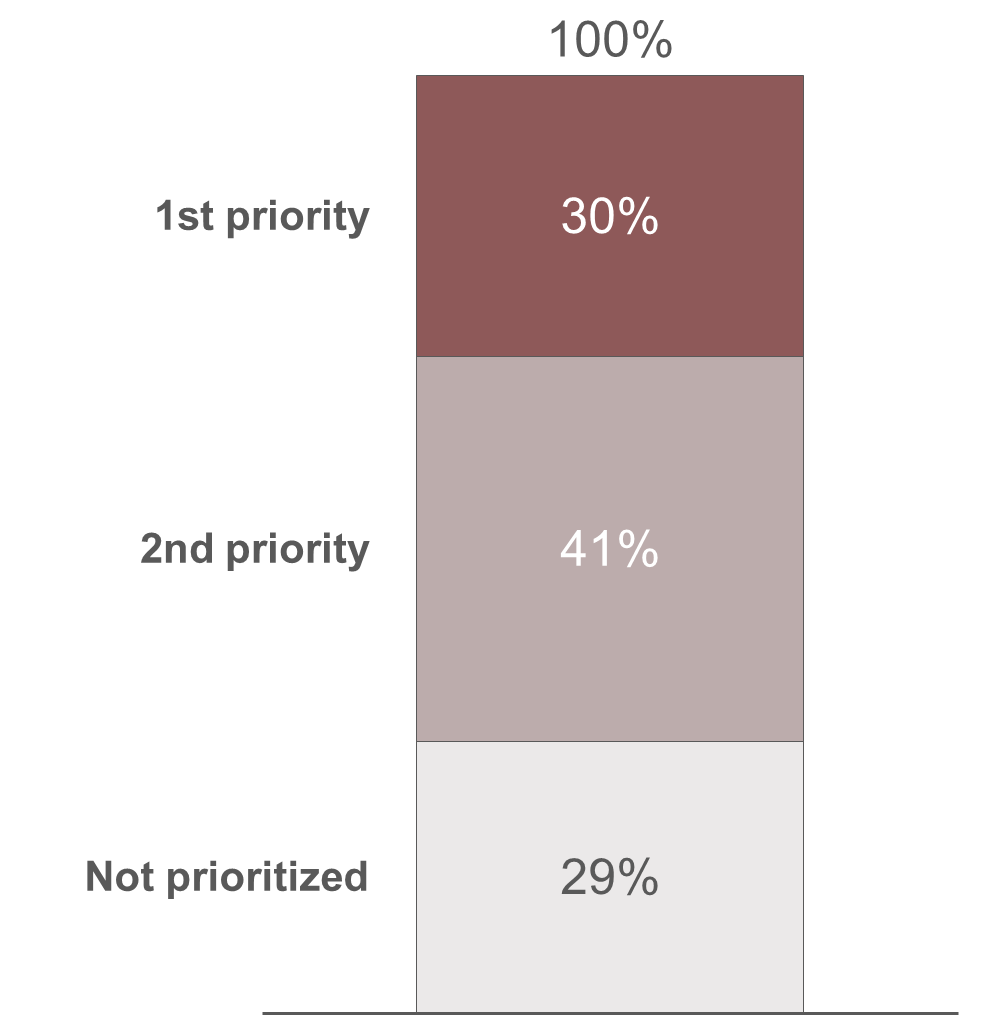

Although focus on indirect costs has increased in recent years, it still is not on top of most companies’ management agenda, and a major review is not a priority despite the size of the cost base, see Figure 2 below. Thus, the potential for cost reductions is significant.

UNCLEAR OWNERSHIP, DECENTRALIZED PROCESS

In some indirect cost categories, e.g. office supplies, ownership of costs may be unclear. Purchases are made by several different parts of a company and overall control is often limited.

In addition, the level of maturity in how purchasing is done can be low and, in many cases, there are no procedures and processes in place. This can lead to volume benefits not being fully exploited or not making use of competitive tendering.

QUICK IMPACT

In addition to the savings potential, the time aspect makes indirect costs attractive from a profitability perspective. Many initiatives have immediate profitability impact or with a relatively short lead time, e.g. by eliminating certain purchases altogether or renegotiating prices.

LEVERS TO REDUCE COSTS

There are several levers to be pulled to achieve reduced indirect costs, examples include:

- renegotiation, competitive tendering

- volume reduction

- simplified requirements

- changed sourcing strategy

- introduction of purchasing policies & procedures

In order to maximize impact, the approach for each measure and category is adapted to its current context. Often a combination of the example methods above is used, e.g. competitive tendering combined with simplified requirement specifications.

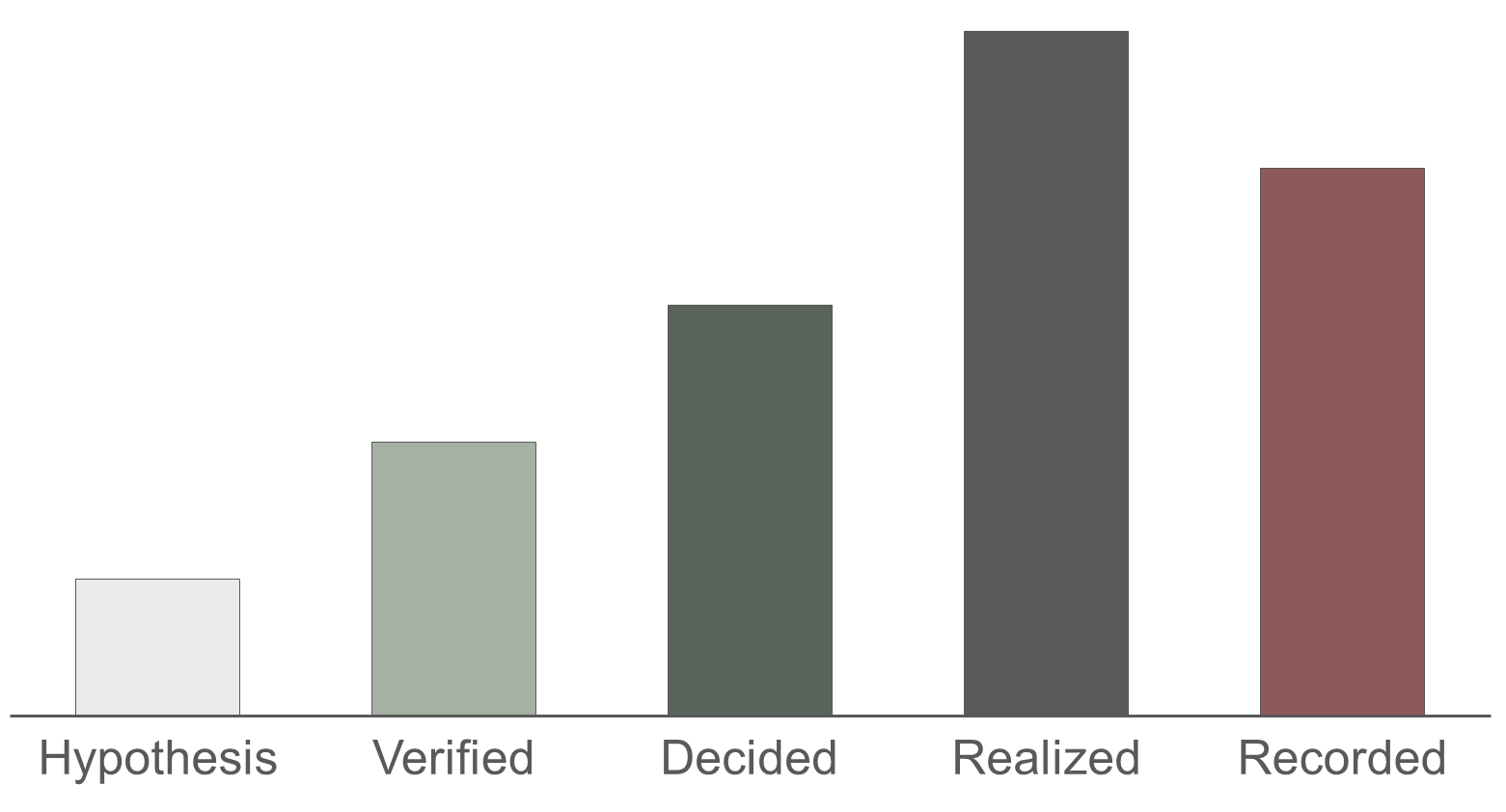

ACTUAL COST SAVINGS

Once saving measures have been implemented, it is important to ensure that the results lead to a real reduction in costs. Once there is room in the budget, it is not uncommon to use the money saved to buy something else that might be “good to have”.

With Axholmen’s simple and structured approach, see Figure 3 below, savings can be monitored and reflected in the budget.